We use cookies to enhance your browsing experience, serve personalized content, and analyze our traffic.

By clicking "Accept All", you consent to our use of cookies. See our

Privacy Policy

for more information.

Economic Laws for Business Strategy: Principles Every Executive Must Know

January 23, 2026Wasil Zafar180 min read

Comprehensive guide to economic laws across 16 strategic categories—from market dynamics and innovation to platforms, negotiation, risk management, macroeconomics, regulation, and labour markets/immigration—that drive pricing, scaling, competitive advantage, and strategic decision-making across every business function.

Every business decision—from pricing strategies to hiring plans, from market entry to product launches—is fundamentally an economic decision. Yet many executives lack a systematic framework for applying economic principles to business strategy. This comprehensive guide bridges that gap by connecting 103+ timeless economic laws to modern business practice, organized into 16 strategic categories spanning market fundamentals, innovation, platforms, negotiation, risk management, macroeconomics, regulation, and labour markets/immigration.

Why Economic Laws Matter for Business

Economic laws aren't abstract theories—they're practical frameworks that explain why certain strategies work and when they fail. Understanding these laws helps executives:

Let's explore each law with real-world examples from companies like Amazon, Tesla, Netflix, Apple, and leading startups, then provide actionable frameworks for executives and business teams across all functions.

CATEGORY A: CORE MARKET & PRICING LAWS

Fundamental laws governing supply, demand, pricing power, and market equilibrium

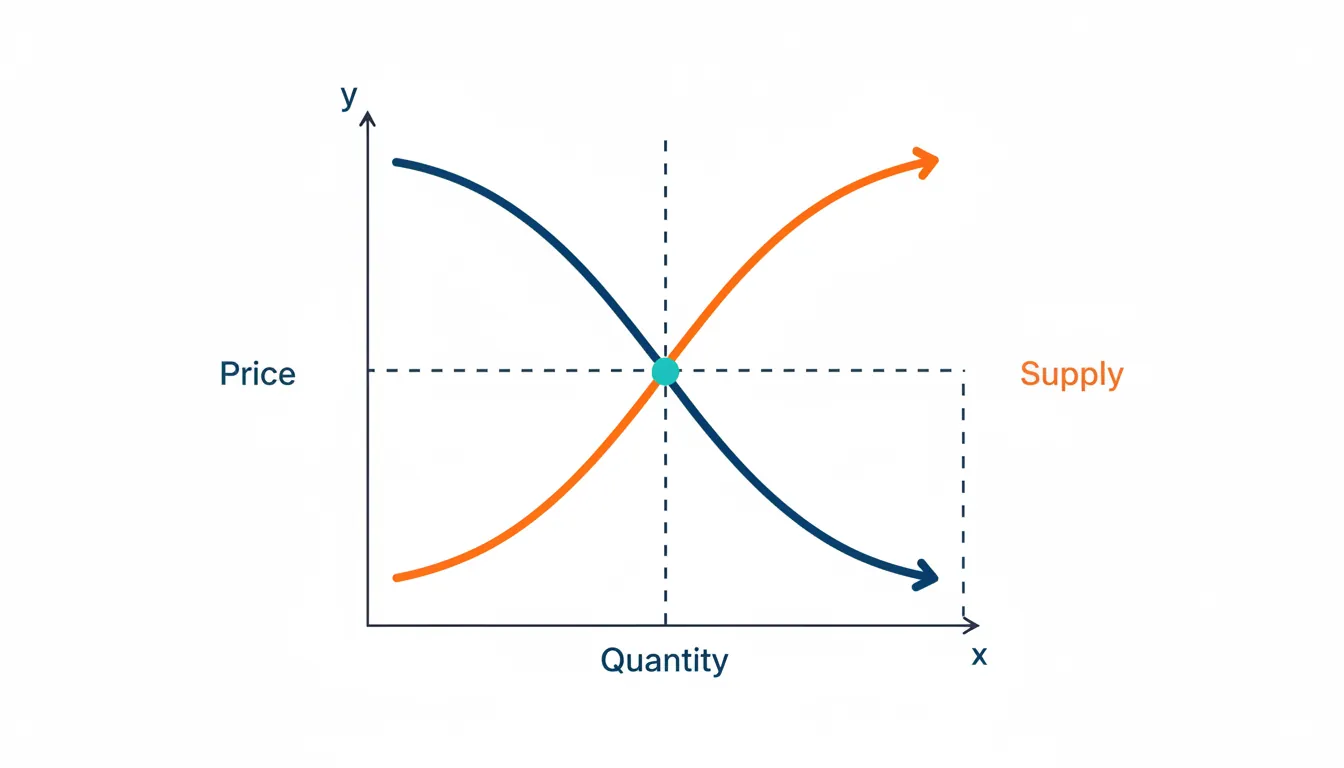

1. Law of Demand & Supply: The Foundation of Pricing

Core Principle: When supply exceeds demand, prices fall. When demand exceeds supply, prices rise. The equilibrium price occurs where supply equals demand.

The law of demand and supply showing equilibrium price at the intersection of supply and demand curves

Real-World Application: Airline Dynamic Pricing

Case Study

Delta Airlines: Demand-Based Revenue Management

Challenge: Fixed capacity (seats per flight) with fluctuating demand patterns

Strategy: Dynamic pricing based on real-time demand signals:

Low demand periods (Tuesday 2pm): Prices drop 40-60% to fill empty seats

High demand (Friday evening, holidays): Prices surge 200-300%

Advance booking: Lower prices when demand uncertainty is high

Last-minute booking: Premium prices for urgent business travel

Result: Revenue per available seat mile (RASM) increased 15-20% through demand-based pricing algorithms

Demand & SupplyPrice Elasticity

Business Applications

For Product Teams: Use A/B testing to find demand curves—test price points to identify where revenue maximizes (price × quantity). Don't assume lower prices always increase total revenue.

For Marketing Teams: Demand generation shifts the demand curve right (more willing buyers at every price). Focus on creating urgency and scarcity when supply is genuinely limited.

For Finance Teams: Model scenario planning around supply shocks (raw material shortages) and demand shocks (competitor moves, economic downturns). Build pricing flexibility into contracts.

Common Mistake: Ignoring supply constraints when stimulating demand. Marketing campaigns that succeed too well can destroy customer satisfaction if you can't fulfill orders. Amazon's early lesson: Don't promote what you can't ship in 2 days.

Amazon's Supply-Demand Mastery

Strategic Example

Amazon Web Services (AWS): Elastic Supply Model

Innovation: Created infinite supply elasticity through cloud infrastructure

Traditional hosting: Fixed capacity = supply shortages during traffic spikes

AWS auto-scaling: Supply expands/contracts with demand in real-time

Pricing model: Pay-per-use eliminates waste from over-provisioning

Business Impact: AWS became a $90B business by solving the supply-demand mismatch in computing

2. Law of Diminishing Returns: When More Becomes Less

Core Principle: Adding more of one input (while holding others constant) eventually yields smaller marginal increases in output. The first engineer adds huge value; the 50th adds incrementally less.

Real-World Application: Startup Hiring Mistakes

Case Study

Scaling Too Fast: The 2021 Tech Hiring Bubble

Context: Tech startups raised massive rounds in 2020-2021 and hired aggressively

Engineers 51-100: 20% productivity (bureaucracy, duplicated work, communication chaos)

2022-2023 Reality Check: Meta, Amazon, Google, Twitter cut 10-20% of workforce—recognizing diminishing returns had set in

Lesson: Growth in headcount ? growth in output. Organizational complexity grows faster than linear headcount.

Diminishing ReturnsEconomies of Scale

Business Applications

For Operations Teams: Measure marginal productivity. If adding the 5th person to a project doesn't increase output by at least the cost of their salary, you've hit diminishing returns. Use small, autonomous teams (Amazon's "two-pizza teams").

For Marketing Teams: Track cost per acquisition (CPA) by channel. The first $100K in Google Ads might yield $500K revenue; the next $100K might only yield $120K. Know when to stop scaling a channel and diversify.

For Finance Teams: Model marginal ROI for capital investments. A factory expansion might have 30% ROI, but the second expansion might only yield 12%. Compare to alternative uses of capital.

Setup: 2016-2017, Uber aggressively recruits drivers in major cities. San Francisco: first 5,000 drivers = 95% utilization (high rider demand, instant pickup). Added 5,000 more drivers (10,000 total) = 70% utilization (more competition for rides). Added another 10,000 (20,000 total) = 40% utilization (drivers waiting 30+ minutes between rides).

Diminishing Returns Impact: First 5,000 drivers: each earns $30/hour (busy constantly). Next 5,000: each earns $20/hour (more idle time). Next 10,000: each earns $12/hour (barely above minimum wage). Marginal productivity declining sharply—too many drivers chasing same rider demand. Driver churn spikes from 15% monthly to 40% monthly as earnings drop.

Key Insight: Adding more supply (drivers) hits diminishing returns when demand (riders) doesn't scale proportionally. Uber learned to model "optimal driver density" per market—beyond this point, adding drivers hurts both driver income and company efficiency (paying incentives to recruit drivers who then quit due to low earnings).

Quantifying Diminishing Returns Formula: Marginal Product = Change in Output ÷ Change in Input Decision Rule: Continue adding resources while Marginal Revenue > Marginal Cost Warning Sign: When marginal product falls below average product, you're over-investing

3. Law of Opportunity Cost: The Hidden Price of Every Decision

Core Principle: The true cost of any choice is what you give up by not choosing the next-best alternative. Money spent on Project A cannot be spent on Project B.

2005 Decision: Launch Prime with free 2-day shipping for $79/year

Opportunity Cost Analysis:

What Amazon gave up: $1-2 billion in annual shipping revenue

Alternative use of capital: Could have built 10 new fulfillment centers

Short-term impact: Profit margins compressed 3-5%

What Amazon Gained:

200M+ Prime members paying $139/year = $28B recurring revenue

Prime members spend 2-3x more than non-Prime customers

Customer lifetime value increased 5-10x

Lesson: Bezos chose long-term customer lock-in over short-term profits. The opportunity cost was worth it.

Opportunity CostTime Value of Money

Business Applications

For Strategy Teams: Every "yes" to a new initiative is a "no" to something else. Use a decision matrix that explicitly lists trade-offs. Ask: "What are we NOT doing because we're doing this?"

For Product Teams: Feature prioritization is opportunity cost management. Building Feature A means delaying Feature B. Use ROI ranking: Value ÷ (Cost + Opportunity Cost).

For HR Teams: Hiring one VP of Sales means you can't hire a VP of Product this quarter. Model the revenue impact of each role's first year. Choose the higher NPV option.

Executive Decision Framework

Before any major decision, answer three questions:

What is the explicit cost? (Money, time, resources)

What is the opportunity cost? (Next-best alternative foregone)

What is the total cost? (Explicit + Opportunity)

Only proceed if Total Value > Total Cost

4. Law of Price Elasticity: Understanding Pricing Power

Core Principle: Elasticity measures how much quantity demanded changes when price changes. High elasticity = price-sensitive customers (commodities). Low elasticity = pricing power (luxuries, necessities).

Real-World Application: Luxury vs. Budget Airlines

Comparative Analysis

Inelastic Demand: Business Class Travel

Elasticity: -0.3 (relatively inelastic)

10% price increase: Only 3% decrease in bookings

Why: Corporate travelers don't pay out-of-pocket, value comfort/time

Result: Airlines can charge $3,000 for a seat that costs $400 in economy

Margin: Business class generates 50-70% of airline profits despite 10% of passengers

Elastic Demand: Budget Airlines (Spirit, Ryanair)

Elasticity: -2.5 (highly elastic)

10% price increase: 25% decrease in bookings

Why: Leisure travelers extremely price-sensitive, have alternatives (driving, trains)

Strategy: Ultra-low base fares + ancillary fees (bags, seats, snacks)

Result: Can't raise prices without losing customers—must compete on cost efficiency

Price ElasticityCompetition

Factors That Reduce Elasticity (Increase Pricing Power)

For Pricing Teams: Segment customers by elasticity. Charge high prices to inelastic segments (enterprise), low prices to elastic segments (SMBs). Use versioning (Basic/Pro/Enterprise) to capture both.

For Marketing Teams: Reduce elasticity through differentiation. Generic product = high elasticity. Branded product with unique features = low elasticity. Invest in branding to reduce price sensitivity.

For Sales Teams: Identify switching costs. If a prospect has high switching costs from their current vendor, you must offer 30-50% more value to justify the change. Conversely, defend your own customers by increasing switching costs (integrations, custom features, data lock-in).

Setup: Starbucks operates 35,000+ stores globally with regional pricing power. US market: premium positioning (coffee + "third place" experience), price inelastic. Emerging markets (China, India): more price sensitive, elastic demand.

Elasticity Test Results: US stores: 2018-2023 raised prices 5% annually (accumulated 28% increase over 5 years). Customer count declined 2% total (very inelastic, elasticity = -0.07). Revenue per store increased 25% (price increases > volume declines). China stores: 2019 test 8% price increase ? 12% traffic decline (elastic, elasticity = -1.5). Revenue declined 5% (price increases < volume losses). Reversed price increase, focused on store expansion instead.

Strategic Implication: Same brand, different elasticity by market. US: brand loyalty, lack of substitutes (independent coffee shops closed during COVID), habit formation = inelastic. Can raise prices aggressively. China: intense competition (Luckin Coffee 10,000+ stores, cheaper alternative), emerging middle class price-sensitive = elastic. Must compete on value. Starbucks adapts pricing strategy to local elasticity: US focus on price realization (raise prices, premiumize), China focus on volume growth (affordable pricing, rapid expansion to 9,000 stores by 2025).

Testing Price Elasticity Formula: Elasticity = (% Change in Quantity) ÷ (% Change in Price) Elastic (>1): Revenue falls when price rises ? lower prices to maximize revenue Inelastic (<1): Revenue rises when price rises ? raise prices to maximize revenue Unit Elastic (=1): Revenue unchanged when price changes ? optimize for other factors

5. Cross Elasticity of Demand: Understanding Product Substitution

Core Principle: Cross elasticity measures how demand for Product A changes when the price of Product B changes. Positive cross elasticity = substitutes (Coke vs. Pepsi). Negative cross elasticity = complements (printers vs. ink).

When Disney+ launched at $6.99: Netflix saw 15% churn increase in households with children

Why: Both offer streaming video, similar content types, easy to switch

Business Impact: Netflix had to invest billions in original content to differentiate

Result: Price war—Netflix couldn't raise prices without losing customers to Disney+

Low Substitution: Spotify vs. Apple Music

Cross Elasticity: +0.3 (weak substitutes)

Why low: Playlists, algorithms, social features create switching costs

User behavior: Once users invest time curating Spotify, they stay despite price increases

Strategic lesson: Build features that reduce cross elasticity with competitors

Cross ElasticityCompetition

Business Applications

For Product Teams: Build features that reduce substitutability. Proprietary data formats, integrations, network effects—anything that makes switching costly. Salesforce's AppExchange (10,000+ apps) makes it hard to switch to competitors.

For Pricing Teams: Monitor competitor pricing closely when cross elasticity is high. In commodity markets (gasoline, airline tickets), match competitor price changes within hours or lose share immediately.

For Strategy Teams: Map your competitive landscape by cross elasticity. High cross elasticity = intense price competition. Low cross elasticity = pricing power. Invest in differentiation to reduce cross elasticity.

Cross Elasticity Decision Framework Formula: Cross Elasticity = (% Change in Qty of A) ÷ (% Change in Price of B) Substitutes (Positive): When competitor raises price, your demand increases Complements (Negative): When complement's price rises, your demand falls Example: When gas prices rise, demand for SUVs falls (complements)

6. Income Elasticity of Demand: Economic Cycles & Consumer Behavior

Core Principle: Income elasticity measures how demand changes when consumer income changes. Normal goods (elasticity > 0) see demand rise with income. Inferior goods (elasticity < 0) see demand fall as income rises.

Real-World Application: Recession-Proof vs. Cyclical Businesses

2021 Recovery: Revenue surged 60% as incomes rebounded

Strategic implication: Luxury brands are highly cyclical—need cash reserves for downturns

Staples: Low Income Elasticity (+0.2)

Example: Walmart, Dollar General, generic brands

2008 Recession: Walmart revenue grew 7% while Target fell 3%

Why: People still need groceries, household goods regardless of income

Strategic advantage: Recession-resistant business model attracts stable investors

Inferior Goods: Negative Income Elasticity (-0.5)

Example: Instant ramen, used cars, public transportation

Recession boom: Nissin (instant noodles) revenue up 25% in 2008-2009

Recovery decline: As incomes recovered, consumers switched to fresh food

Income ElasticityMarket Cycles

Business Applications

For Finance Teams: Use income elasticity to forecast revenue during economic cycles. High elasticity = volatile revenue, need larger cash reserves. Low elasticity = stable revenue, can operate with higher leverage.

For Strategy Teams: Portfolio diversification by income elasticity. Luxury conglomerate LVMH owns both high-elasticity brands (Louis Vuitton) and low-elasticity brands (Sephora cosmetics) to smooth revenue cycles.

For Marketing Teams: Adjust messaging by economic climate. Recession: emphasize value, durability, necessity. Boom: emphasize status, aspiration, premium features.

Income Elasticity Strategy Matrix

Product Category

Income Elasticity

Recession Strategy

Luxury (+2 to +4)

Very High

Build cash reserves, cut costs fast, focus on ultra-wealthy

Normal Goods (+0.5 to +1.5)

Moderate

Shift to value messaging, introduce economy tiers

Necessities (0 to +0.5)

Low

Maintain prices, gain market share from premium brands

Inferior Goods (-0.5 to -2)

Negative

Increase production, recession is growth opportunity

7. Law of Scarcity: Artificial Limits & Psychological Value

Core Principle: Scarcity increases perceived value. Limited availability creates urgency and demand, even when artificial. Humans value rare items more than abundant items, regardless of utility.

The law of scarcity showing how limited availability drives up perceived value and consumer urgency

Drop model: New items every Thursday, sell out in minutes

Limited quantities: Typical drop = 300-500 units per item (vs. 100,000+ for normal retail)

No restocks: Once sold out, item never returns

Result: $20 t-shirt resells for $200+ on secondary market

Business Impact:

Brand value: Supreme sold to VF Corp for $2.1B (2020)

Margin: 60-70% gross margin (vs. 40% for normal apparel)

No discounting: Items never go on sale—scarcity maintains value

Free marketing: Scarcity creates FOMO, drives organic social buzz

ScarcityPricing Power

Types of Strategic Scarcity

Scarcity Type

Example

Business Mechanism

Quantity Scarcity

Limited editions, numbered prints

Nike's limited sneaker drops, Hermès Birkin bags

Time Scarcity

Flash sales, seasonal items

Amazon Prime Day, McDonald's McRib

Access Scarcity

Waitlists, invite-only

Gmail beta (2004), Clubhouse invites (2020)

Geographic Scarcity

Regional exclusives

Tesla only in select cities initially

Business Applications

For Product Teams: Design scarcity into product launches. Gmail's invite-only beta (2004-2007) created massive demand despite free alternatives (Yahoo, Hotmail). Scarcity = exclusivity = desirability.

For Marketing Teams: Use countdown timers, "Only X left in stock," and limited-time offers. Booking.com's "Only 1 room left!" messaging increases conversion 15-25% through urgency.

For Sales Teams: Create artificial scarcity through limited allocations. SaaS companies use "Limited beta slots available" to speed up enterprise sales cycles from 9 months to 3 months.

Scarcity Warnings & Best Practices Ethical Use: Don't fake scarcity—customers will discover truth and backlash (e.g., fake countdown timers that reset) Product-Market Fit First: Scarcity amplifies desire for good products, doesn't create demand for bad ones Balance: Too much scarcity = lost revenue (Supreme leaves money on table). Too little = no urgency Best Formula: Produce 70-80% of potential demand to create scarcity without maximizing revenue loss

CATEGORY B: CHOICE, VALUE & INVESTMENT LAWS

Laws governing strategic trade-offs, decision-making, and value maximization

8. Law of Comparative Advantage: Build vs. Buy Decisions

Core Principle: Focus on activities where you have the lowest opportunity cost, even if you're not the absolute best at them. Outsource everything else.

Last-mile delivery: Increasingly using third-party drivers (Uber model)

Decision Framework: Build if (1) core competency, (2) strategic moat, (3) cheaper at scale. Otherwise buy.

Comparative AdvantageEconomies of Scale

Business Applications

For Strategy Teams: Map your value chain. For each activity, ask: "Are we 10x better than best-in-class vendors?" If no, consider outsourcing. Focus resources on the 2-3 activities that create competitive moats.

For Product Teams: Buy vs. build frameworks for features. Use third-party APIs for non-core features (payments, auth, analytics). Build proprietary features that differentiate you. Stripe succeeded by letting companies outsource payment infrastructure.

For HR Teams: Hire for comparative advantage. Don't hire a $200K engineer to do $50K ops work. Use contractors/offshore for tasks without strategic value. Reserve full-time hires for core competencies.

Background: In March 2018, Trump imposed 25% tariffs on steel imports and 10% on aluminum, citing national security. The policy aimed to protect domestic steel/aluminum producers from foreign competition, particularly from China.

Classical Comparative Advantage Prediction:

China specialization: Lower labor costs, economies of scale ? comparative advantage in steel production

US specialization: Higher productivity in tech, aerospace, finance ? comparative advantage in capital-intensive industries

Free trade outcome: US imports steel cheaply, focuses resources on high-value sectors ? both countries gain

Tariff Impact (Violating Comparative Advantage):

Effect

Outcome

Data

Import Volume

Steel imports dropped

Down 15% (2018-2019)

Domestic Prices

Steel prices rose sharply

+30% spike (2018)

Protected Jobs

Steel industry jobs increased

+8,700 jobs

Downstream Job Losses

Manufacturers paid more for steel

-75,000 jobs (est.)

Consumer Impact

Higher prices (cars, appliances, construction)

+$900/household/year

Trade Diversion

Companies sourced from Vietnam, Mexico instead

40% import shift

Retaliation

EU, China, Canada imposed counter-tariffs

$13B US exports targeted

Economic Analysis:

Deadweight loss: Tariffs created inefficiency ? resources shifted from efficient uses (tech, services) to inefficient steel production. Net cost: $7.2B/year (higher prices + job losses - protected jobs)

Terms of trade manipulation: Attempted to force China to lower export prices, but retaliation offset gains

Who paid the tariff: US consumers and manufacturers, not Chinese exporters (inelastic demand ? passed through as higher prices)

Job opportunity cost: $900,000 per steel job saved (could have retrained workers for $50K ? massive inefficiency)

Key Insight: Protectionism violates comparative advantage ? both countries worse off. Short-term political gains (visible jobs saved) masked larger invisible costs (consumer prices, downstream job losses, retaliation). Free trade maximizes total welfare; tariffs redistribute gains (to protected industry) while creating deadweight loss (net economic harm).

Comparative AdvantageProtectionismDeadweight Loss

2025 Update: Trump's Second Term Tariff Escalation

Current Policy2025-2026

Continuation and Expansion of Protectionist Strategy

Background: Upon assuming office in January 2025, Trump immediately resumed aggressive tariff policy, building on 2018-2020 precedents but with broader scope. Key actions (January 2025-January 2026):

Economic prediction: Tariff burden split between consumers and foreign producers based on demand/supply elasticity

Actual incidence (2025 data): US consumers/businesses paying 92-95% of tariff costs (similar to 2018-2020)

Why: Inelastic demand for many imports (semiconductors, rare earths, specialized machinery) + rapid trade diversion to third countries limits foreign exporters' pricing power

Household impact: Average +$2,100/year in higher costs (vs. $1,277 in 2018-2020) due to broader tariff scope

4. Retaliation & Game Theory (Prisoner's Dilemma Intensified):

Counter-measures (2025-2026): China: 60% tariffs on US ag exports, rare earth export restrictions. EU: €250B in retaliatory tariffs (Boeing, agriculture, tech). Mexico: 25% on US corn, machinery (USMCA violations alleged)

Escalation spiral: Each round of tariffs triggers counter-tariffs ? both sides worse off but locked in by domestic politics

Global impact: World trade growth: -1.5% (2025), projected -2.8% (2026) due to uncertainty and fragmentation

5. Trade Diversion (Inefficient Substitution):

Pattern: Rather than producing in US, companies shift sourcing to third countries (Vietnam, India, Indonesia, Thailand)

2025 data: Chinese exports to US: -$180B. Vietnam/India exports to US: +$95B. US domestic production increase: +$12B only

Efficiency loss: Vietnam/India often less efficient than China for many products ? higher global production costs (consumer harm) without US job creation

Example: iPhone production shifting to India (30% higher labor costs, lower productivity) ? retail prices up 8-12%

Real-World Implications (2025-2026):

Sector

Impact

Winners

Losers

Manufacturing

Input costs up 20-30%

Domestic steel/aluminum producers (+15,000 jobs)

Auto manufacturers, construction, machinery (-90,000 jobs)

Mexico border enforcement: Tariff threats to force cooperation on immigration ? Mexico deployed 30,000 troops to northern border, increased enforcement

EU defense spending: Auto tariff threats conditional on NATO spending increases ? partial success (Germany committed 2.5% GDP target)

China fentanyl crackdown: 60% tariff leverage to force drug precursor controls ? limited compliance

Market Disruptions:

Stock market volatility: S&P 500 down 15% (Q1 2025) on tariff announcements, recovered 8% on exemption news ? policy whiplash

Currency moves: Dollar strengthened 12% vs Yuan (tariff-driven), weakened 6% vs Euro (retaliation concerns) ? FX instability

Supply chain chaos: Companies scrambling to relocate production, renegotiate contracts ? $80B in restructuring costs (Fortune 500)

Investment freeze: Business CapEx down 18% (2025) due to policy uncertainty ? delayed expansion, hiring

Key Insight (2025-2026 Era): Trump's second-term tariff policy demonstrates systematic manipulation of foundational economic principles. Comparative advantage rejected (forced domestic production regardless of efficiency). Price mechanism distorted (tariffs override market signals). Elasticity ignored (claimed foreigners pay tariffs, data shows 92%+ falls on Americans). Game theory misapplied (assumed unilateral threats work, triggered mutual retaliation). Trade diversion over creation (shifted supply chains to third countries, minimal US production gains).

Political Economy Calculation: Concentrated benefits (visible manufacturing jobs: +15,000) vs. dispersed costs (invisible consumer harm: +$2,100/household × 130M households = $273B). Policy persists because winners (steel workers, domestic producers) are vocal and organized, while losers (all consumers) bear small individual costs and don't mobilize. Classic public choice problem: protectionism survives despite negative net welfare impact because benefits are concentrated and costs are diffuse.

Long-Term Consequences: Fragmentation of global supply chains (US-China decoupling accelerating), higher structural inflation (tariff-driven cost-push), reduced innovation (R&D budgets cut to offset tariff costs), geopolitical tensions (trade wars escalate to tech/investment restrictions), allies alienated (EU, Mexico, Canada relations strained). Net economic cost: -0.8% GDP growth (2025-2026) per consensus estimates, with long-term productivity losses from inefficient resource allocation.

2025 TariffsTrade War EscalationPolicy ManipulationEconomic Distortion

9. Law of Diminishing Marginal Utility: Why More Isn't Always Better

Core Principle: The satisfaction (utility) gained from each additional unit of consumption decreases. First slice of pizza = amazing. Fifth slice = less enjoyable. Tenth slice = negative utility (pain).

Real-World Application: SaaS Pricing Tiers

Pricing Strategy

How Slack Captures Value Through Marginal Utility

Free Tier: High marginal utility per feature

10,000 searchable messages: Huge value for small teams

SAML SSO, compliance exports: Zero value for SMBs, critical for enterprise

24/7 support: Most users never need, but enterprises require

Strategy: Price on willingness-to-pay, not utility (enterprise can afford it)

Marginal UtilityPrice Discrimination

Business Applications

For Product Teams: Design good/better/best tiers based on marginal utility curves. Front-load high-utility features in basic tier to drive adoption. Reserve low-utility features for premium tiers—charge high prices because alternatives are expensive (build custom SSO vs. pay for Business+ tier).

For Marketing Teams: Message marginal benefits correctly. Don't oversell features with low marginal utility—customers won't pay. Focus messaging on high-utility differentiators.

For Finance Teams: Revenue optimization = maximize area under marginal utility curve. Tiered pricing captures different utility segments—free tier (first units, high utility), pro tier (middle units, moderate utility), enterprise tier (last units, low utility but high willingness-to-pay).

Diminishing Marginal Utility in Action Freemium Model: Gives away high-marginal-utility features free ? customers hooked ? pay for moderate-utility features Subscription Fatigue: 15th streaming service has near-zero marginal utility ? churn increases Decision Rule: Stop adding features when marginal cost > marginal utility for target customer

10. Sunk Cost Fallacy: When to Cut Your Losses

Core Principle: Sunk costs are past expenses that cannot be recovered. Rational decision-making ignores sunk costs and focuses only on future costs/benefits. Yet humans irrationally factor sunk costs into decisions ("I've already invested so much...").

Real-World Application: Google Glass & Strategic Pivots

Failure Analysis

When Google Fell for Sunk Cost Fallacy (Initially)

2012-2014: Sunk Costs Accumulate

R&D Investment: $500M+ in hardware, software, partnerships

Team Size: 50+ engineers, designers, product managers

Marketing: Super Bowl ads, celebrity endorsements

Market signal: Terrible reception—called "Glassholes," privacy concerns, no product-market fit

Pivoted to enterprise: Refocused on warehouses, factories (actual use case)

Key insight: Ignored sunk costs, made decision based on future prospects

Contrast: If trapped by sunk costs, would've poured another $500M into doomed consumer product

Sunk Cost FallacyStrategic Pivots

Common Sunk Cost Traps in Business

Business Context

Sunk Cost Trap

Rational Response

Failed Product

"We've spent $10M building this, we can't give up now"

If future expected value < future costs, shut it down regardless of past spend

Underperforming Employee

"We invested 2 years training them, can't fire now"

Past training is sunk. If current output < current cost, replace

Bad Acquisition

"We paid $1B, must make it work"

Acquisition price is sunk. If integration costs > expected value, divest

Legacy Tech Stack

"We've customized this CRM for 10 years"

Past customization is sunk. If migration cost < (old TCO - new TCO), migrate

Business Applications

For Strategy Teams: Quarterly portfolio review—ask "If we were starting today, would we invest in this project?" If no, shut it down regardless of sunk costs. Amazon's "two-way door" framework: easily reversible decisions should be made fast, ignoring sunk costs.

For Finance Teams: Use incremental analysis for go/no-go decisions. Only factor in future cash flows. Spreadsheet discipline: never include past expenditures in NPV calculations for continuing projects.

For Product Teams: Feature deprecation based on future maintenance cost vs. future value, not past development cost. Slack sunset Slack Connect features that cost $5M to build but had low engagement—right call despite sunk cost.

Setup: 2011 Netflix: 24M DVD subscribers, $2B invested in DVD distribution infrastructure (58 fulfillment centers, automated sorting machines, logistics network). DVD business highly profitable: $3.2B revenue, 52% operating margins. But streaming emerging: 22M streaming subscribers, growing 60% annually.

Sunk Cost Decision: Reed Hastings (CEO) faces choice: (1) Protect DVD business (slow streaming investment, maximize cash from existing infrastructure), or (2) Cannibalize DVD, accelerate streaming (write off $2B infrastructure over 5 years, invest heavily in streaming content/tech). Wall Street pressures protection of profitable DVD segment. Hastings chooses cannibalization despite massive sunk costs.

Execution: 2011: Netflix splits DVD/streaming into separate services ($15.98/month combined ? $7.99 each if separated). Customer backlash: 800,000 subscribers cancel (stock drops 75%). But strategy: force customers to choose streaming or DVD—accelerate streaming adoption, starve DVD business. 2012-2016: DVD subscribers decline 20M ? 3M. Netflix stops investing in DVD infrastructure, deploys $15B into streaming content (House of Cards, Orange is New Black, international expansion).

Result: 2024: Netflix 260M streaming subscribers, $33B revenue, $280B market cap. DVD business shut down July 2023 (final 1M subscribers). Key lesson: Hastings ignored sunk costs ($2B DVD infrastructure) and opportunity costs (foregone DVD profits) to capture streaming future. Blockbuster made opposite choice—protected $6B retail store infrastructure (sunk cost fallacy), refused to cannibalize. Result: bankruptcy (2010). Sunk cost discipline = competitive advantage.

Sunk Cost Decision Framework Question: "If I had not already invested X, would I invest it now?" If Yes: Continue project (but base decision on future prospects, not past investment) If No: Exit project immediately (sunk costs are irrelevant) Red Flag: Phrases like "We've come too far to quit now" or "Can't waste what we've invested"

11. Risk-Return Tradeoff: No Free Lunch in Finance

Core Principle: Higher potential returns require taking higher risk. Low-risk investments offer low returns. Cannot have both high returns and low risk—markets are efficient at pricing risk.

Real-World Application: Startup vs. Corporate Job

Career Decision

The Risk-Return Spectrum of Career Paths

Low Risk, Low Return: Corporate Job at Fortune 500

Salary: $120K base + $30K bonus = $150K total comp

10-year outcome: $1.5M-$2M total earnings, high certainty

High Risk, High Return: Early-Stage Startup

Salary: $80K base + 0.5% equity = expected value ~$100K year 1

Risk: 90% chance of failure (startup fails, equity worthless)

10-year outcome: 90% chance = $800K total earnings. 10% chance of $10M+ (IPO/acquisition)

Expected value: (0.9 × $800K) + (0.1 × $10M) = $1.72M (similar to corporate, but much higher variance)

Risk-ReturnExpected Value

Business Applications

For Finance Teams: Capital allocation by risk-return profile. Conservative companies (utilities, banks) invest in low-risk, low-return projects (bonds, blue-chip stocks). Growth companies (tech startups) swing for high-risk, high-return bets (R&D, acquisitions).

For Strategy Teams: Portfolio approach to risk. Don't bet entire company on one high-risk project—70% low-risk projects (sustaining innovations), 20% medium-risk (adjacent markets), 10% high-risk (breakthrough innovations). Google's "70-20-10" rule.

For Investors: Startup investing requires power law thinking. Most investments fail (0x return), few succeed (3-5x), rare home runs (100x+). Need portfolio of 20+ investments to achieve statistical edge. Single high-risk bet = gambling, not investing.

Risk-Return Matrix for Business Decisions

Risk Level

Expected Return

Example Investment

Low Risk

5-8% annual

Treasury bonds, savings accounts, core business operations

Medium Risk

10-15% annual

S&P 500 index, adjacent market expansion, product line extensions

High Risk

20-30%+ annual (or total loss)

Startups, new product categories, international expansion, M&A

CATEGORY C: COST, PRODUCTION & SCALING LAWS

Laws governing production efficiency, cost structures, and scaling dynamics

12. Returns to Scale: When Doubling Inputs Doesn't Double Output

Core Principle: Returns to scale describe what happens to output when you proportionally increase all inputs. Increasing returns = output more than doubles. Constant returns = output exactly doubles. Decreasing returns = output less than doubles.

Scenario: Double infrastructure investment (servers, data centers, networking)

Double inputs (cost): $100B ? $200B total infrastructure

More than double output (capacity): Better server utilization (80% vs. 60%), bulk purchasing discounts (40% cheaper per unit), shared services (one global CDN serves 2x customers)

Result: 2.5x capacity increase for 2x cost increase = increasing returns to scale

Strategic advantage: Scale becomes an unbeatable moat—no competitor can match AWS economics without matching scale

Returns to ScaleEconomies of Scale

Business Applications

For Operations Teams: Identify if your business has increasing returns to scale. Software yes (zero marginal cost). Professional services no (linear scaling). Manufacturing maybe (depends on automation vs. labor mix).

For Strategy Teams: In industries with increasing returns to scale, prioritize market share over short-term profitability. First mover advantage is massive—Amazon poured billions into AWS infrastructure when unprofitable, now has 32% market share and 70%+ margins.

For Finance Teams: Model scale scenarios carefully. Decreasing returns to scale = diseconomies emerging (bureaucracy, complexity). Signal to split into smaller units or divest non-core assets.

Identifying Returns to Scale Type Increasing Returns: Software, platforms, networks (fixed costs dominate) Constant Returns: Retail, franchises (replicable business model) Decreasing Returns: Custom services, creative work (key resources don't scale) Red Flag: If scaling from 100 ? 200 employees makes coordination harder, you're hitting decreasing returns

13. Learning Curve Effect: Experience as Competitive Advantage

Core Principle: As cumulative production volume doubles, unit costs decline by a constant percentage (typically 10-30%). Not about time—about repetition. Experience makes you more efficient.

Real-World Application: Tesla Battery Cost Decline

Manufacturing Excellence

How Tesla Achieved 90% Battery Cost Reduction

2010 Roadster (first 2,500 units):

Battery cost: $1,000/kWh

Manufacturing approach: Manual assembly, high defect rates

Cumulative learning: Every doubling of production ? 20% cost reduction

Strategic Moat:

Tesla's 5M+ cumulative vehicle production = decades of learning curve advantage

New EV startups (Lucid, Rivian) start at 2010 Tesla cost levels—can't compete on cost until they achieve similar scale

Learning CurveManufacturing

Business Applications

For Operations Teams: Track learning curve rate for your production processes. Plot log-log chart of cumulative volume vs. unit cost. Slope = learning rate. Use this to forecast future costs at higher volumes.

For Strategy Teams: First mover advantage in manufacturing-heavy industries comes from learning curve, not innovation. Boeing vs. Airbus—decades of production experience = cost advantage new entrants can't match without producing similar cumulative volumes.

For Pricing Teams: Price aggressively early to gain volume, move down learning curve faster than competitors. Once cost advantage achieved, raise prices—competitors can't match profitability. Classic strategy: penetration pricing ? volume ? learning ? cost leadership ? margin expansion.

Learning Curve Formula & Strategy Formula: Y = aX^b (where Y = unit cost, X = cumulative volume, b = learning rate) Typical Rates: Aerospace (80% - every doubling = 20% cost reduction), Electronics (70%), Services (90%) Strategic Implication: Industries with steep learning curves (70-80%) favor early movers and high-volume producers Decision Rule: If learning rate <85%, prioritize volume growth over margins in early years

14. Economies of Scope: Leveraging Shared Resources

Core Principle: Economies of scope occur when producing multiple products together is cheaper than producing them separately. Shared resources (infrastructure, brand, distribution, R&D) reduce average cost per product.

Real-World Application: Amazon's Business Model

Scope Economics

How Amazon Leverages Shared Infrastructure

Shared Resource: Fulfillment Network

Retail: Stores and ships Amazon.com orders

FBA (Fulfillment by Amazon): Same warehouses fulfill third-party seller orders

External product: Sold to enterprises as AWS ($90B revenue)

Scope synergy: R&D costs amortized across 2 customer bases

Shared Resource: Brand & Customer Base

Prime membership: Drives adoption of Prime Video, Music, Reading

Cross-sell: Customer who joins for fast shipping subscribes to video ? no new customer acquisition cost

Economies of ScopePlatform Strategy

Business Applications

For Product Teams: Identify shared resources that can power multiple products. Shopify's merchant dashboard powers online stores, POS, payments, shipping—one codebase, multiple revenue streams.

For Strategy Teams: M&A based on scope economies. Disney bought Marvel, Star Wars, Pixar—shared distribution (Disney+), shared merchandising, shared theme park attractions. Each IP is more valuable in Disney's portfolio than standalone.

For Finance Teams: Calculate scope economies through joint cost allocation. If producing A+B together costs less than producing A alone + B alone, scope economies exist. Quantify synergy value in acquisition models.

Economies of Scope vs. Economies of Scale Scale: Lower cost per unit as volume increases (more of same thing) Scope: Lower cost per product as variety increases (more different things using shared resources) Example: Walmart has scale (bulk purchasing), Amazon has scope (shared fulfillment) Best Strategy: Combine both—shared platform (scope) serving high volume (scale)

15. Law of Increasing Complexity: When Growth Creates Chaos

Core Principle: As organizations grow, complexity increases exponentially (not linearly). Communication pathways = n(n-1)/2 where n = people. 10 people = 45 connections. 100 people = 4,950 connections. Coordination costs can overwhelm productivity gains.

Real-World Application: The Two-Pizza Team Rule

Organizational Design

Amazon's Solution to Complexity Explosion

The Problem: Large Teams Slow Down

5-person team: Ship feature in 2 weeks, minimal meetings, direct communication

20-person team: Ship same feature in 8 weeks—4x slower despite 4x resources

Principle: Team should be small enough to feed with two pizzas (~6-8 people)

Autonomy: Each team owns full feature/service, minimal dependencies

APIs: Teams interact through documented interfaces, not meetings

Result: Reduced complexity—10 small teams outship 1 large team of 100

Evidence of Complexity Costs:

Brooks's Law: "Adding engineers to late project makes it later" (coordination > productivity)

Mythical Man-Month: 9 women can't have a baby in 1 month—some work doesn't parallelize

ComplexityOrganizational Design

Business Applications

For Leadership Teams: Combat complexity through org design. Spotify's "squads and tribes" model, Valve's flat hierarchy, Basecamp's 3-person teams—all minimize coordination overhead. Don't solve problems by adding people—solve by reducing dependencies.

For Operations Teams: Simplify processes as you scale. Each process decision = permanent complexity tax. Amazon's "mechanisms not meetings" philosophy—replace recurring coordination with automated systems.

For Product Teams: Modular architecture reduces complexity. Microservices, APIs, plug-in systems—allow teams to work independently. Monolithic codebases require coordination = exponential complexity growth.

Complexity Warning Signs Red Flags:

Decision velocity slowing despite adding people

Meetings proliferating to align stakeholders

Features taking longer to ship as team grows

Email/Slack volume overwhelming workers

Solutions: Split teams, reduce dependencies, automate coordination, eliminate unnecessary work

CATEGORY D: INCENTIVES & ORGANIZATIONS

Laws governing incentive alignment, organizational behavior, and metrics design

16. Law of Incentives: Aligning Behavior with Strategy

Core Principle: People respond to incentives—often in unintended ways. What you measure and reward becomes what people optimize for, not necessarily what you want.

Incentive Design: Sales quotas tied to number of accounts opened per customer

Goal: Increase cross-selling (get customers to use multiple products)

Metric: Accounts per customer (wanted 8 per household)

Rewards: Bonuses, promotions, job security for hitting quotas

Unintended Consequences:

What happened: Employees opened 3.5M fake accounts without customer consent

Why: Metric rewarded quantity over quality, no penalty for fake accounts

Result: $3B in fines, CEO fired, brand destroyed

Lesson: Narrow incentives create narrow optimization. Must align metrics with long-term customer value, not short-term actions.

IncentivesCompetition

Designing Better Incentives

Best Practice

Amazon's Customer Obsession Metrics

Sales Team Incentives:

? Bad metric: Revenue per customer (encourages upselling junk)

? Good metric: Customer lifetime value (CLV) - repeat purchase rate

Customer Service Team:

? Bad metric: Calls resolved per hour (encourages rushing customers)

? Good metric: Customer satisfaction score + first-contact resolution

Product Team:

? Bad metric: Features shipped (encourages bloat)

? Good metric: User adoption of features + retention impact

Business Applications

For HR/Compensation Teams: Audit all incentive structures quarterly. Ask: "If employees maximally optimize for this metric, what's the worst thing that could happen?" Test incentives with small pilots before rolling out company-wide.

For Sales Teams: Balance short-term metrics (quarterly revenue) with long-term metrics (customer retention, expansion revenue). Weight compensation 60/40 between the two. Punish bad revenue (high churn accounts).

For Leadership: Culture is what you incentivize, not what you say. If you preach collaboration but reward individual performance, you'll get silos. Measure and reward team outcomes.

Incentive Design Checklist

Before implementing any incentive system:

Alignment: Does it drive the behavior we actually want?

Gaming: How could someone game this metric unfairly?

Unintended consequences: What could go wrong if maximized?

Balance: Do we incentivize both quality and quantity?

Long-term: Does it reward sustainable vs. extractive behavior?

17. Goodhart's Law: When Measures Become Targets

Core Principle: "When a measure becomes a target, it ceases to be a good measure." People optimize for the metric instead of the underlying goal, often with perverse outcomes.

The Metric: Cross-sell Ratio (accounts per customer)

Original intent: Measure customer satisfaction and product fit

Became target: Employees judged and compensated on cross-sell numbers

Gaming behavior: Opened 3.5M+ fake accounts without customer permission

Why gaming worked: Metric went up, actual value (customer relationships) went down

Consequences:

Fines: $3B in regulatory penalties

Stock crash: 30% drop in market cap ($35B loss)

CEO resignation: John Stumpf forced out

Lesson: Optimizing for the wrong measure destroys value faster than creating it

Goodhart's LawMetrics Design

Business Applications

For Leadership Teams: Design metrics that are hard to game. Instead of "lines of code" (easily gamed by writing bloated code), use "features shipped that customers use." Instead of "calls handled" (incentivizes rushing), use "issues resolved on first call."

For HR Teams: Avoid single-metric performance reviews. Netflix doesn't track hours worked—managers judge output and impact. Google's OKRs separate ambitious goals (60-70% achievement expected) from performance reviews (prevents gaming by setting easy goals).

For Product Teams: Be skeptical of vanity metrics. "Daily active users" can be gamed by annoying notifications. Better metric: "engaged users who find value" (harder to fake). Goodhart's Law explains why MAU is often misleading—companies game it through spam.

Preventing Goodhart's Law Strategy 1: Use multiple complementary metrics (can't game all simultaneously) Strategy 2: Measure leading indicators AND lagging outcomes Strategy 3: Rotate metrics periodically (prevents long-term gaming) Strategy 4: Qualitative checks alongside quantitative targets (manager discretion)

18. Principal-Agent Problem: Misaligned Interests

Core Principle: The principal-agent problem occurs when one party (agent) makes decisions on behalf of another (principal), but their interests don't align. Classic example: shareholders (principals) vs. executives (agents).

Real-World Application: Executive Stock Options

Alignment Strategy

How Stock Comp Aligns Principal-Agent Interests

The Problem: Executives' Incentives ? Shareholders' Interests

Shareholders want: Long-term value creation, sustainable growth

Salaried execs want: Job security, short-term targets, empire building

Conflict: Exec might reject risky but valuable projects to protect their job

Solution: Stock Options with Vesting

Grant: CEO receives options for 1M shares at $50/share

Vesting: 25% per year over 4 years (must stay to realize value)

Alignment: If stock hits $100, CEO makes $50M (same 2x return as shareholders)

Result: CEO now incentivized to take smart risks that grow company value

Remaining Problems:

Short-termism: Options can incentivize pumping stock before vesting, then dumping

Risk-taking: Options have asymmetric payoff—huge upside, limited downside (can't go below zero)

Better solution: Restricted stock units (RSUs) that align on downside too

Principal-AgentIncentive Design

Common Principal-Agent Problems in Business

Context

Principal

Agent

Misalignment

Solution

Corporate Governance

Shareholders

Executives

Execs prioritize perks, job security over shareholder value

For HR Teams: Design compensation to align interests. Sales reps on commission optimize for closing deals (agent interest). Add customer retention bonuses to align with company's long-term interest (principal).

For Strategy Teams: Recognize when you're the agent, not the principal. Consultants (agents) are paid for recommendations, not results—creates incentive to recommend expensive projects regardless of ROI. Solution: tie fees to implementation success.

For Investors: Due diligence on management alignment. How much stock do founders own? What's the vesting schedule? Are there super-voting shares? Misaligned management = avoid investment.

Solving Principal-Agent Problems Alignment: Make agent's financial outcomes depend on principal's success Monitoring: Regular audits, transparency requirements, oversight boards Incentives: Bonuses tied to long-term metrics, deferred compensation Competition: Multiple agents competing reduces individual power to exploit principal

19. Parkinson's Law: Work Expands to Fill Time

Core Principle: "Work expands so as to fill the time available for its completion." Give someone 1 hour for a task, they'll finish in 1 hour. Give them 1 week, they'll take the full week. Organizational corollary: bureaucracies grow regardless of actual workload.

Real-World Application: Government vs. Startup Efficiency

For Project Managers: Set aggressive deadlines. Amazon's "working backwards" from launch date forces teams to cut scope, not extend timelines. Tight deadlines = creative problem-solving. Loose deadlines = bikeshedding and feature creep.

For Leadership Teams: Combat bureaucratic expansion. Parkinson observed that bureaucracies grow 5-7% annually regardless of workload. Solution: zero-based budgeting (justify every headcount from scratch), regular org reviews, flat hierarchies.

For Product Teams: Time-boxing decisions. Basecamp's "6-week cycles" force teams to ship something in fixed time. Can't extend deadline ? must cut scope or ship MVP. Prevents perfectionism and over-engineering.

Counteracting Parkinson's Law Tight deadlines: Create artificial urgency (ship before conference, beat competitor launch) Resource constraints: Limited budget forces prioritization Public commitments: Announcing launch date creates accountability Incremental delivery: Ship MVPs ? prevents work from expanding indefinitely

20. Peter Principle: Rising to Your Level of Incompetence

Core Principle: "In a hierarchy, people tend to rise to their level of incompetence." Great engineers get promoted to engineering managers (different skillset), great salespeople become sales managers (now bad at their job). Result: organizations fill management ranks with incompetent people.

Real-World Application: The Manager Track Trap

Career Trap

How Companies Lose Great Individual Contributors

Scenario: Top Software Engineer

IC Level 5: Excellent engineer, ships critical features, loves coding

Promotion to Manager: Only path to higher pay/status in most orgs

New role: Now spends 80% time in meetings, performance reviews, hiring—zero coding

Outcome: Company loses great engineer, gains mediocre manager (no management training or aptitude)

Peter Principle in action: Rose to level of incompetence (management)

Solution: Dual Career Tracks (Google, Meta, Netflix)

IC track: Staff Engineer ? Senior Staff ? Principal ? Distinguished (equivalent to Director ? VP)

Manager track: Engineering Manager ? Senior EM ? Director ? VP

Result: Top engineers can earn $500K+ without managing anyone—no forced incompetence

Peter PrincipleCareer Ladders

Business Applications

For HR Teams: Create parallel career tracks. Let people progress in their area of competence. Microsoft's IC track goes to "Technical Fellow" (reports to CEO, $1M+ comp)—no need to switch to management to advance.

For Leadership Teams: Promote based on fit for next role, not performance in current role. Great salesperson ? great sales manager. Require management training before promotion, trial periods as "acting manager," or rotate people back to IC roles if management doesn't work out.

For Individuals: Recognize your zone of genius. If you love individual contribution (coding, design, writing), don't take management job for title/money. Negotiate for IC advancement or leave for company with better IC track.

Preventing the Peter Principle Dual tracks: IC and management paths with equal prestige/compensation Lateral moves: Allow "demotions" without stigma if role isn't working Skills assessment: Promote based on abilities needed for next role, not past performance Management training: Teach skills before promoting, not after failure

CATEGORY E: COMPETITION & MARKET STRUCTURE

Laws governing competitive dynamics, market positioning, and sustainable advantages

21. Law of Competition: The Invisible Hand That Erodes Profits

Core Principle: Perfect competition drives profits to zero. Sustainable profitability requires competitive moats—barriers that prevent rivals from eroding your margins.

Real-World Application: Airline Industry Economics

Industry Analysis

Why Airlines Struggle to Make Money

Perfect Competition Characteristics:

Commodity product: Seat from NYC to LA is identical across carriers

Low switching costs: Customers choose based on price + schedule only

High fixed costs: Planes, gates, staff—costs are same whether full or empty

Easy price comparison: Google Flights shows all options instantly

Result: Competition forces prices down to marginal cost

Industry profit margins: 1-3% (vs. 20-30% for software)

Bankruptcies: Most major airlines filed for Chapter 11 (2000-2010)

Consolidation: Merged down to 4 major carriers to reduce competition

CompetitionEconomies of Scale

Building Competitive Moats

Moat Type

How It Works

Example

Durability

Network Effects

Value increases with users

Facebook, Visa

Very High

Switching Costs

Expensive/painful to leave

SAP, Workday

High

Economies of Scale

Cost advantage from size

Walmart, Amazon

High

Brand/Intangibles

Premium pricing from trust

Apple, Nike

Medium

Regulatory/IP

Legal barriers to entry

Pharma patents, Uber licenses

Medium

Data

Unique dataset others can't replicate

Google Search, Bloomberg

Medium-High

Business Applications

For Strategy Teams: Audit your moats quarterly. Rate each moat 1-10 on strength. If average score < 5, you're vulnerable. Invest aggressively in strengthening moats before competitors erode margins.

For Product Teams: Build features that increase switching costs. Integrations, proprietary data formats, workflows that become muscle memory. Make it painful to leave.

For Sales Teams: In competitive markets, win on relationships and service, not price. Price wars destroy margins. Differentiate on intangibles that justify premium pricing.

Warren Buffett's Moat Test

"The key to investing is determining the competitive advantage of any given company and, above all, the durability of that advantage."

Questions to ask:

If we stopped innovating today, how long until competitors catch up?

What would it cost a new entrant to replicate our position?

Can we raise prices 10% without losing 10% of customers?

How many of our customers would switch if a competitor offered 20% lower prices?

22. Creative Destruction: Innovation That Destroys Incumbents

Core Principle: Innovation creates new industries while destroying old ones. Capitalism's "gale of creative destruction" (Schumpeter) drives economic progress but makes most companies obsolete. Adapt or die.

Creative destruction showing how innovation creates new industries while making established ones obsolete

Real-World Application: Digital Photography Killed Film

Industry Disruption

Kodak's $28B Evaporation

1996: Kodak at Peak

Market cap: $28B, 145,000 employees

Dominance: 70% US film market share, household name globally

Irony: Kodak invented digital camera in 1975 but buried it (cannibalized film business)

2012: Kodak Bankrupt

Digital photography: Smartphones made cameras ubiquitous (iPhone 4S outsold all Kodak cameras)

Revenue collapse: Film sales fell 90% in 10 years

Creative destruction winner: Canon, Sony, and ultimately Apple/Samsung captured $200B+ camera phone market

Kodak mistake: Protected dying business (film) instead of cannibalizing it with digital

Creative DestructionDisruption

Business Applications

For Strategy Teams: Map your "S-curve" lifecycle. Every technology/business model has growth, maturity, decline phases. Netflix destroyed Blockbuster (DVDs ? streaming), then started destroying itself (streaming ? interactive content). Continually innovate before competitors do.

For R&D Teams: Invest in potentially disruptive technologies even if they cannibalize current revenue. Amazon's AWS cannibalized enterprise software sales—but better to cannibalize yourself than let competitors do it. Intel's "next bench" philosophy: always have team working on technology to replace current products.

For Leadership Teams: Cultural willingness to destroy own products. Steve Jobs killed iPod with iPhone ("If we don't cannibalize, someone else will"). Contrast with Microsoft's delay in mobile—protected Windows at expense of smartphone future.

Creative Destruction Strategy Attacker advantage: Startups have nothing to lose—can pursue disruptive tech aggressively Incumbent disadvantage: Protecting existing revenue streams prevents pivoting to new models Solution: Create separate divisions for disruptive innovations (Amazon's AWS started as skunkworks) Decision Rule: If technology could destroy your business in 5-10 years, invest in it TODAY

23. Barriers to Entry: Moats That Protect Profits

Core Principle: Barriers to entry are factors that make it difficult or expensive for new competitors to enter a market. High barriers = sustainable profits. Low barriers = competition erodes margins.

Fab investment: Each new semiconductor fab costs $20B+

R&D spending: $15B+ annually on next-generation processes

Time to replicate: 5-7 years minimum (Moore's Law advancement)

Knowledge barrier: Decades of accumulated manufacturing expertise

Why Barrier Is Weakening:

TSMC, Samsung: Matched Intel's investment, now ahead on 3nm process

Lesson: Capital barriers only work if you maintain technological lead

2024 status: Intel lost manufacturing advantage—barrier eroded by competitors' equal investment

Barriers to EntryCapital Requirements

Business Applications

For Strategy Teams: Build multiple overlapping barriers. One barrier can be overcome (patents expire, regulations change). Combine barriers for durable moat: network effects + economies of scale + brand (e.g., Amazon).

For Startups: Choose markets with low barriers initially, then build barriers after gaining foothold. Software SaaS has low capital requirements (easy to enter) but can build network effects and switching costs over time (hard to displace).

For Investors: Invest in companies with high, durable barriers. Buffett's "wide moat" investing: businesses where competitive advantages are structural, not temporary. Avoid markets where barriers are eroding (newspapers, retail).

Building Durable Barriers Strongest barriers: Network effects (self-reinforcing), regulatory monopolies (government-enforced) Weakest barriers: First-mover advantage alone (easily copied), proprietary tech (expires, reverse-engineered) Best strategy: Combine 2-3 barrier types for defense in depth

24. Winner-Takes-Most Markets: Power Law Distribution

Core Principle: In winner-takes-most markets, the top player captures disproportionate share of profits. Not linear distribution (everyone gets some)—exponential (leader gets 50-90%, everyone else fights for scraps).

Data network effects: More searches ? better algorithm ? more users ? more searches (flywheel)

Advertiser concentration: Advertisers go where users are ? reinforces Google dominance

Default positioning: Google pays Apple $15B+/year to be default iOS search ? locks in users

Switching costs: Low for users, but why switch if Google works best?

Winner-Takes-MostMarket Concentration

Markets That Exhibit Winner-Takes-Most

Market Characteristic

Winner-Takes-Most?

Example

Network effects

? Yes

Social networks, marketplaces, operating systems

High fixed costs, low marginal costs

? Yes

Software, pharmaceuticals, media

Strong brand effects

? Yes

Search, video streaming, cloud

Commoditized products

? No

Agriculture, raw materials, generic drugs

Fragmented preferences

? No

Restaurants, fashion, consulting

High switching costs

?? Maybe

Enterprise software (winner-takes-most within verticals)

Business Applications

For Startups: In winner-takes-most markets, second place is first loser. Prioritize growth over profitability—spend aggressively to win (Uber, DoorDash burned billions racing to dominance). If you can't be #1, don't enter market.

For Investors: Power law portfolio construction. Most startups fail, few become unicorns. In winner-takes-most sectors, returns are extreme—invest in 20+ companies, expect 1-2 to return entire fund (Benchmark's $11M Uber investment ? $7B return).

For Strategy Teams: Recognize when you're in winner-takes-most market and act accordingly. Can't compete on features alone—need network effects, scale advantages, or niche dominance. Example: Zoom focused on ease-of-use to beat Cisco WebEx despite fewer features.

Winner-Takes-Most Strategy If you're #1: Defend position aggressively—pay for exclusivity, undercut on price, acquire threats If you're #2-3: Find defensible niche or merge to achieve scale If you're #4+: Exit market or pivot—long-term viability unlikely Red Flag: Raising more funding to "compete" in winner-takes-most market when already behind

25. Market Power: Pricing Above Marginal Cost

Core Principle: Market power is the ability to raise prices above competitive levels (marginal cost) without losing all customers. Perfect competition = zero market power. Monopoly = maximum market power. Most businesses exist in between.

Real-World Application: Apple's iPhone Pricing Power

Pricing Power Analysis

How Apple Captures 85% of Smartphone Industry Profits

Cost Structure:

iPhone 15 Pro Max: Manufacturing cost ~$500, retail price $1,199

Gross margin: 58% (vs. 10-20% for Android competitors)

Differentiation: iOS ecosystem is genuinely different from Android (not perfect substitute)

Switching costs: Moving to Android means losing iMessage, FaceTime, app purchases

Brand premium: Apple = status symbol, customers willing to pay for logo

Network effects: More iPhone users ? more iMessage groups ? more pressure to stay

Contrast: Commoditized Android Market

Samsung, Xiaomi, OnePlus: Compete mainly on price

Low differentiation: All run Android, similar features

Result: Margins compressed to 10-15%—minimal market power

Market PowerPricing Power

Business Applications

For Product Teams: Build differentiation to gain market power. Commoditized products = no pricing power = race to bottom. Focus on features competitors can't easily copy: brand, design, integration, customer service.

For Pricing Teams: Test pricing power systematically. Raise prices 5-10% on subset of customers, measure churn. If churn < 5%, you have pricing power—keep raising. If churn > 15%, you're commoditized—compete on value, not price.

For Strategy Teams: Monitor market power trends. Increasing competitive pressure = eroding market power = margin compression ahead. Example: Netflix's market power declined as Disney+, HBO Max, Apple TV+ launched—had to cut subscription price growth to retain customers.

Measuring Your Market Power High Market Power Signals:

Gross margins >50% sustained over multiple years

Price increases don't trigger significant churn

Customers complain about price but don't leave

You can dictate terms to suppliers/distributors

Low Market Power Signals:

Can't raise prices without losing customers to competitors

Gross margins <20% and compressing

Customers view you as interchangeable with rivals

You must match competitor pricing instantly

CATEGORY F: SCALE & NETWORK EFFECTS

Laws governing exponential growth, platform dominance, and winner-take-all dynamics

26. Law of Economies of Scale: Size as Strategy

Core Principle: As production volume increases, cost per unit decreases. Larger firms can achieve lower costs through fixed cost spreading, purchasing power, and operational efficiencies.

Logistics network: $50B invested in distribution centers ? 2% logistics cost (vs. 8% for small retailers)

Technology amortization: $10B IT investment spread over $600B revenue = 1.7% of sales

Private label brands: Cuts out middleman, captures 25-40% margin on own brands

Result: 25-30% cost advantage vs. small competitors

Walmart COGS: 75% of revenue

Small retailers COGS: 80-85% of revenue

Implication: Walmart makes profit at prices that bankrupt competitors

Economies of ScaleCompetition

Types of Scale Economies

1. Fixed Cost Spreading: Software companies—$100M development cost spread over 1M users = $100/user. Over 100M users = $1/user. Marginal cost approaches zero.

2. Purchasing Economies: Large buyers negotiate volume discounts. Amazon Web Services gets server hardware 40-60% cheaper than small cloud providers.

3. Learning Curve Effects: Repetition improves efficiency. Tesla's battery cost fell 50% from Model S (2012) to Model 3 (2017) through manufacturing learning.

4. Network Density: Uber's unit economics improve in dense cities. More riders + more drivers = shorter wait times + higher utilization = lower cost per ride.

When Scale Becomes a Disadvantage

Warning

Diseconomies of Scale: When Bigger Is Worse

Bureaucracy: Large orgs require layers of management—decision speed slows

Coordination costs: Communication overhead grows exponentially with team size

Market power limits: Can't raise prices further without triggering anti-trust (Google, Meta)

Innovation inertia: Kodak couldn't pivot to digital despite inventing it—too much invested in film

Tipping point: When marginal coordination cost > marginal scale benefit, split into smaller units

Business Applications

For Operations Teams: Track unit economics by volume tier. Model how costs change at 2x, 5x, 10x current scale. Identify which costs are truly fixed (amortize over more units) vs. variable (scale linearly).

For Finance Teams: Build scale scenarios into pro formas. Show board that path to profitability requires achieving X market share to unlock Y% cost advantage. Justify initial losses as investment in scale.

For Strategy Teams: In winner-take-all markets (high fixed costs, low marginal costs), prioritize market share over profitability early on. Examples: Uber, Spotify, Netflix spent years unprofitable to achieve scale.

Scale Economics Formula Minimum Efficient Scale (MES): Smallest production volume where cost per unit is minimized Decision Rule: If current volume < MES, prioritize growth. If volume > MES, prioritize efficiency. Red Flag: If market size < 3x your MES, market may be too small for sustainable profitability

9. Law of Network Effects: The Ultimate Moat

Core Principle: A product becomes more valuable as more people use it. Unlike traditional goods (pie gets smaller when shared), network goods create exponential value with each new user.

Types of Network Effects

Type

Mechanism

Example

Strength

Direct Network Effects

More users = more value to each user

WhatsApp, Zoom, Email

Very Strong

Two-Sided Marketplaces

More buyers attract sellers, vice versa

eBay, Airbnb, Uber

Very Strong

Data Network Effects

More usage = better product (ML)

Google Search, Waze, Spotify

Strong

Platform Effects

More apps attract users, more users attract apps

iOS, Windows, PlayStation

Very Strong

Social Network Effects

Value from connections (friends/followers)

Facebook, LinkedIn, Twitter

Very Strong

Real-World Application: Facebook's Dominance

Network Effects Case

Why Facebook Crushed MySpace and Google+

Network Effect Flywheel:

2004-2007: College students join ? their friends must join to connect

Critical mass: At 50M users, new user's friends likely already on platform

Tipping point: At 100M users, NOT being on Facebook means social isolation

Switching costs: Your photos, posts, friend graph = years of data lock-in

Why Competitors Failed:

MySpace (2008): Users left for Facebook ? their friends followed ? MySpace lost critical mass

Google+ (2011): Better product, but no one's friends were there ? dead on arrival

Lesson: Can't beat network effects with features alone—need to solve cold start problem

Network EffectsCompetition

Building Network Effects: The Cold Start Problem

Chicken-and-Egg Challenge: Platforms need both sides (buyers + sellers, users + content creators) but neither will join without the other.

Strategies to Solve Cold Start:

Startup Playbook

How Successful Platforms Bootstrapped

1. Single Side First (Airbnb):

Founders manually recruited hosts by photographing apartments

Built supply (listings) first, then drove demand through Craigslist arbitrage

Once 100+ quality listings in NYC, word-of-mouth took over

2. Fake the Other Side (Reddit):

Founders created fake user accounts to post content

Made site appear active to attract real users

Real users joined, created content, attracted more users

3. Subsidize One Side (Uber):

Paid drivers guaranteed hourly wage to ensure supply

Offered free rides to riders to create demand

Lost money until critical mass achieved, then scaled back subsidies

4. Niche ? Expand (Facebook):

Started at single college (Harvard) ? achieved 100% penetration

Expanded college-by-college ? critical mass in each before moving on

Network effects strong within each college, then interconnected

Business Applications

For Product Teams: If building a marketplace, solve single-side value first. Uber = good for drivers even without riders (reliable taxi business). Airbnb = hosts could list on Craigslist too. Don't build pure platforms without single-player utility.

For Growth Teams: Viral coefficient must be > 1.0 for exponential growth. Measure K-factor: (Invites per user) × (Conversion rate). Dropbox's referral program: 35% of users invited friends, 20% converted = K = 0.07. Needed incentives (free storage) to hit K > 1.

For Strategy Teams: Network effects create winner-take-all markets. Second place gets exponentially less value. Go all-in to achieve critical mass or don't enter at all. Half-measures lose to full commitment.

Network Effect Litmus Test

Ask: "Does the 100th user make the product more valuable to the 1st user?"

Yes: You have network effects (Facebook, Uber, Marketplace)

No: You have scale economies, not network effects (Netflix—more users don't improve my experience)

True network effects are rare but nearly unbeatable when achieved.

28. Power Law Distribution: 80/20 Rule on Steroids

Core Principle: Power law distributions follow the principle that a small number of occurrences account for the majority of outcomes. Unlike normal distributions (bell curve), power laws are heavily skewed—top 1% often captures 50%+ of total value.

Real-World Application: Venture Capital Returns

Portfolio Analysis

Why VCs Need 100x Winners

Typical VC Fund: 30 Investments

20 investments (67%): Total loss or minimal returns (0-1x)

7 investments (23%): Modest returns (2-5x)

2 investments (7%): Strong returns (10-20x)

1 investment (3%): Home run (50-100x+) — THIS ONE RETURNS THE ENTIRE FUND

Example: Sequoia's WhatsApp Investment

Investment: $60M across multiple rounds

Exit: Facebook acquisition for $19B (Sequoia's share: $3B+)

Return: 50x — one investment returned 3x the entire $1B fund

Power law in action: 1 out of 200+ companies generated 300% of fund's profits

Power LawVenture Capital

Business Applications

For Strategy Teams: Identify which of your activities follow power law distributions. Customer value: 20% of customers generate 80% of revenue (focus retention there). Product features: 20% of features drive 80% of usage (prioritize those). Employee performance: Top 10% generate 50%+ of value (retain/clone them).

For Sales Teams: Account prioritization by power law. Enterprise sales: top 100 accounts may generate more revenue than next 10,000 combined. Allocate sales resources accordingly—dedicated account managers for top 1%, inside sales for the rest.

For Product Teams: Power law of user engagement. Most users are inactive, small percentage are power users. Design for power users (they drive retention/revenue), make product accessible for casual users (they drive acquisition).

Power Law vs. Normal Distribution Normal Distribution: Averages meaningful (height, test scores)—most people near middle Power Law: Averages meaningless (wealth, book sales)—extreme outcomes dominate Implication: In power law domains, focus on outliers, not averages. Median startup outcome = failure. But top 0.1% = trillion-dollar companies. Decision Rule: If power law applies, use portfolio approach—many small bets to find rare winners

CATEGORY G: GAME THEORY & STRATEGIC INTERACTION

Laws governing competitive strategy, negotiation, and strategic decision-making

29. Nash Equilibrium: When No One Can Improve by Changing

Core Principle: A Nash equilibrium occurs when each player's strategy is optimal given the other players' strategies. No player has incentive to unilaterally change their strategy. Predicts stable outcomes in competitive situations.

Nash equilibrium: Both Best Buy and competitors keep prices high

Why: If Walmart lowers price, Best Buy automatically matches ? Walmart gains no customers ? no incentive to cut price

Result: Prices stabilize at higher level than without price-matching

Nash EquilibriumGame Theory

Business Applications

For Strategy Teams: Map Nash equilibria in your competitive landscape. Understanding stable outcomes helps predict competitor behavior. If price war has no equilibrium (both lose), rational competitors avoid it—unless disrupting incumbent is worth short-term losses.

For Pricing Teams: Find pricing equilibria where no one benefits from changing. Avoid situations where you're incentivized to undercut but so is competitor—leads to margin erosion with no winner.

Identifying Nash Equilibrium Test: Given competitor's current strategy, can I improve my outcome by changing mine? If Yes: Not at equilibrium—expect strategy shifts If No: Nash equilibrium—stable state (for better or worse)

30. Dominant Strategy: The Obvious Best Move