We use cookies to enhance your browsing experience, serve personalized content, and analyze our traffic.

By clicking "Accept All", you consent to our use of cookies. See our

Privacy Policy

for more information.

Negotiation & Risk Management: 10 Laws for Strategic Flexibility

January 24, 2026Wasil Zafar50 min read

Master deal economics, uncertainty management, and strategic optionality—building flexibility into decisions when the future is unknowable. Part 7 of our 8-part Economics for Business Strategy series.

Introduction: The Economics of Deals and Uncertainty

Every business deal involves uncertainty, incomplete information, and the possibility of opportunistic behavior. How do you structure partnerships when you can't anticipate every contingency? When should you walk away from negotiations? How do you preserve strategic flexibility when the future is unknowable? These questions sit at the intersection of negotiation theory, contract economics, and risk management.

These 10 laws cover deal economics (BATNA, hold-up problems, incomplete contracts) and uncertainty management (real options, Black Swan thinking, optionality). From M&A transactions to strategic partnerships to venture capital investments, understanding these principles separates value-creating deals from value-destroying commitments.

Deal Economics: Using BATNA to strengthen negotiating positions and structure win-win agreements

Contract Design: Managing hold-up problems, incompleteness, and renegotiation dynamics

Transaction Costs: When to make versus buy, insource versus outsource, integrate versus partner

Strategic Flexibility: Applying real options theory to preserve optionality and manage irreversible commitments

Uncertainty Management: Distinguishing risk from Knightian uncertainty and preparing for Black Swan events

Let's begin with the foundational concept in negotiation theory: your best alternative to a negotiated agreement.

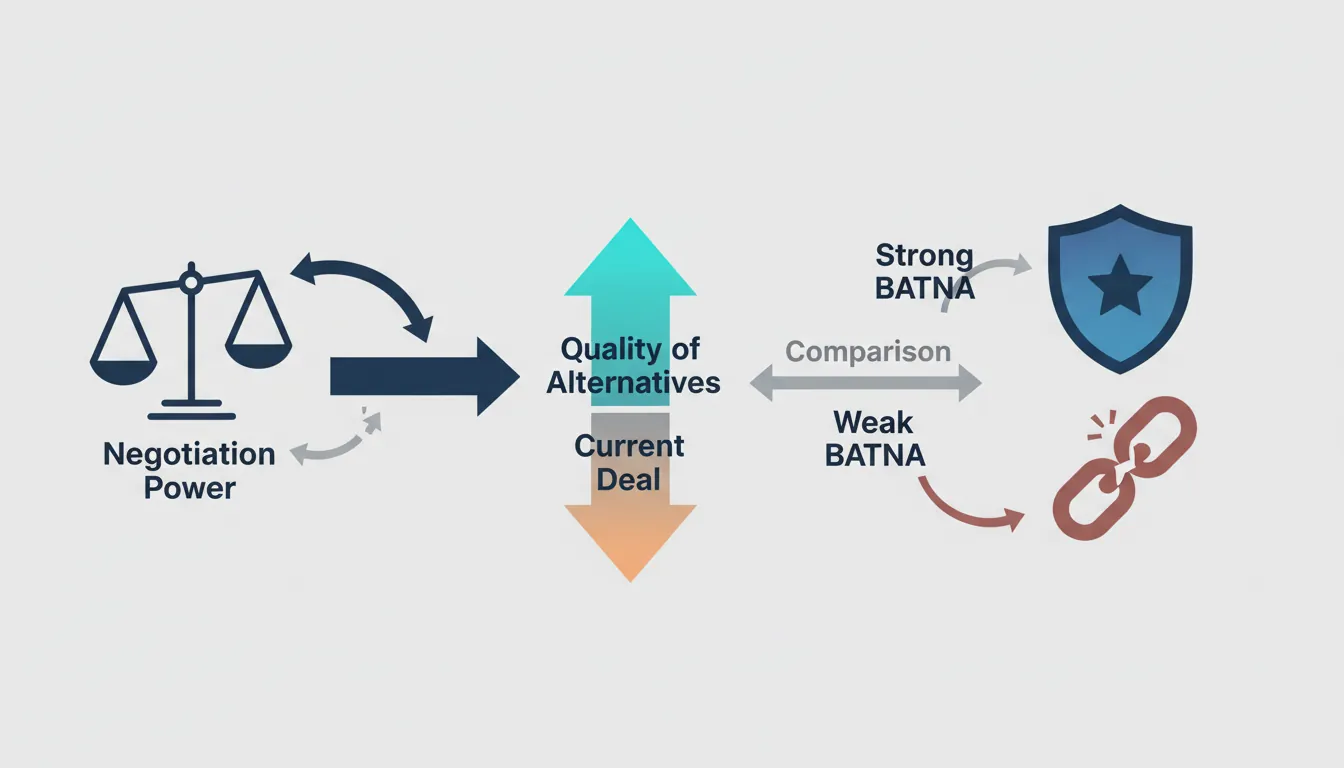

BATNA: Best Alternative Defines Power

Core Principle: Your negotiation power equals your Best Alternative To a Negotiated Agreement (BATNA). Strong BATNA = walk away easily, demand better terms. Weak BATNA = accept worse terms or lose deal. Negotiation outcome determined less by arguments, more by alternatives.

BATNA framework showing how negotiation power is determined by the quality of available alternatives

Negotiation Dynamics: Facebook's weak BATNA: tried competing, couldn't win. Instagram growing faster than Facebook among young users—existential threat. Facebook's BATNA value: -$5B (estimated future market share loss if Instagram becomes competitor). Instagram's strong BATNA: stay independent, worth $5B+ in 5 years (correct—worth $100B+ standalone by 2020). Result: Instagram negotiated up from $1B to $1B + retention bonuses + autonomy guarantees.

Key Insight: BATNA determines who has leverage. Facebook had urgency (competitive threat), Instagram had patience (growing fast, didn't need acquisition). Negotiation power = quality of alternatives, not quality of arguments.

Business Applications

For Negotiators: Improve your BATNA before negotiating. Fundraising: get multiple term sheets (competition improves terms). Enterprise sales: build relationships with multiple vendors (alternatives create leverage). Employment: interview at competitors before asking for raise (outside offers improve BATNA). Never enter negotiation with single option—creates desperation, destroys leverage.

For Dealmakers: Assess counterparty's BATNA. If they have strong alternatives, you must offer competitive terms. If weak alternatives (sole-source vendor, urgent timeline, no competitors), you can demand premium pricing. Salesforce selling to company with homegrown CRM (strong BATNA = keep building internally) must show ROI. Selling to company with outdated legacy CRM (weak BATNA = massive migration pain regardless of vendor) can charge premium.

For Procurement Teams: Create competition to improve BATNA. Multi-vendor RFPs generate competing bids (better pricing than sole-source). Even if preferred vendor known, soliciting alternatives creates pricing pressure. "We're considering Vendor A and Vendor B" changes negotiation dynamics from "will you buy?" to "how do we win against competitor?"—shifts power to buyer.

BATNA Optimization Framework Identify your BATNA: What's your best option if this deal fails? (stay independent, choose competitor, build in-house, walk away) Improve your BATNA: Create alternatives before negotiating (solicit competing offers, develop internal capabilities, extend runway) Assess their BATNA: Research counterparty's alternatives (are they desperate? do they have options? what's their timeline?) Worsen their BATNA: Make alternatives less attractive (exclusive partnerships, FUD about competitors, time pressure) Never reveal weak BATNA: If desperate, don't show it—act like you have strong alternatives even if you don't

Negotiation StrategyDeal LeverageM&A Strategy

Hold-Up Problem: Post-Investment Opportunism

Core Principle: After making relationship-specific investment (can't be redeployed), counterparty exploits your lock-in by demanding better terms. Classic example: build factory near customer's plant (specificity), customer renegotiates lower prices (hold-up). Solved through long-term contracts, vertical integration, or hostage exchanges.

Real-World Application: Supplier Relationships

Case Study: Auto Parts Supplier Vulnerability

ManufacturingHold-Up Problem

Setup: Parts supplier agrees to build custom components for auto manufacturer. Invests $50M in specialized equipment, molds, testing rigs. Equipment only works for this specific car model—can't repurpose for other customers.

Hold-Up: After supplier invests $50M (sunk cost), manufacturer says: "We're re-evaluating supplier contracts. Accept 20% price cut or we'll source elsewhere." Supplier's dilemma: accept cut (loses $10M/year margin) or refuse (loses $50M investment + all future revenue). Manufacturer exploiting specific investment—supplier locked in, has no alternatives. Classic hold-up problem.

Solutions: (1) Long-term contract BEFORE investment (5-year commitment, price protection). (2) Vertical integration (manufacturer owns supplier). (3) Hostage exchange (supplier also manufactures parts for manufacturer's competitor—mutual lock-in). Toyota pioneered "relational contracts"—long-term partnerships, invest in supplier success, avoid hold-up opportunism.

Business Applications

For Procurement Teams: Use hold-up leverage strategically but carefully. Short-term: exploiting supplier lock-in saves costs. Long-term: suppliers won't invest in innovation/capacity if fearing hold-up. Result: stagnant supply chain, quality declines. Smart approach: long-term contracts with performance incentives (share gains from innovation, don't extract all surplus through renegotiation). Costco's supplier model: consistent volume guarantees, fair pricing, suppliers invest in Costco-specific packaging/logistics knowing hold-up won't occur.

For Partnership Teams: Protect against hold-up through contract design. If making specific investment (custom integration, dedicated team, infrastructure), negotiate: (1) Minimum volume commitments (guarantees ROI), (2) Price escalation clauses (inflation protection), (3) Termination penalties (counterparty pays for stranded investment if canceling early). AWS enterprise contracts: 3-year commitments, minimum spend thresholds, protect AWS from hold-up after customer migrates all infrastructure.

For Strategy Teams: Vertical integration vs. outsourcing decision driven by hold-up risk. High relationship-specificity + uncertain demand = vertical integrate (avoid hold-up). Low specificity + certain demand = outsource (standard contracts work). Apple designs chips in-house (high specificity—custom ARM architecture) but outsources manufacturing to TSMC (standard fabrication, multiple customers, low hold-up risk). Tesla vertically integrated batteries (high specificity, critical to performance) but outsources seats (commodity, many suppliers).

Preventing Hold-Up Problems Long-term contracts: Lock in prices/terms BEFORE specific investment Vertical integration: Own both sides (eliminate counterparty opportunism) Hostage exchange: Mutual specific investments (both locked in, balanced power) Reputation effects: Repeated relationships (hold-up damages future deal flow) Contract clauses: Minimum volume commitments, termination penalties, price escalation protection Warning: Hold-up opportunism profitable short-term, destroys partnerships long-term

Incomplete Contracts: Not All Futures Can Be Written

Core Principle: Contracts can't specify actions for every possible future state (too complex, too expensive, some states unforeseen). Parties must govern relationship through trust, reputation, and renegotiation. Governance structure (joint venture, partnership, employment) determines how unspecified situations resolved.

Real-World Application: Joint Ventures

Case Study: Starbucks-PepsiCo Bottled Frappuccino JV

Unspecified States: What if customer wants low-calorie version? (Starbucks wants to protect brand, PepsiCo wants market share). What if Coca-Cola offers Starbucks better distribution deal? (PepsiCo wants exclusivity, Starbucks wants competition). What if almond milk becomes popular? (recipe change requires both parties' approval—who decides?). Contract can't predict all future product innovations, competitive dynamics, consumer preferences. Parties must renegotiate constantly.

Governance: Joint venture board (3 Starbucks directors, 3 PepsiCo directors) resolves disputes. Works because: (1) Repeated interaction (long-term partnership, reputation matters), (2) Mutual dependence (Starbucks needs PepsiCo's distribution, PepsiCo needs Starbucks' brand), (3) Symmetric information (both have full visibility into operations). JV governance structure handles incompleteness better than rigid contract.

Business Applications

For Legal Teams: Accept that contracts are inherently incomplete. Don't try to specify every contingency (infinite legal fees, still won't cover everything). Focus on: (1) Governing principles (how disputes resolved, who has decision rights), (2) Termination conditions (exit if relationship fails), (3) Renegotiation process (how often terms revisited, trigger events). Spotify's podcast creator contracts: specify revenue share, content ownership, but leave creative decisions to creators (too many edge cases to prespecify).

For Partnership Teams: Choose partners with aligned incentives and reputation for fairness. If contract incomplete (it always is), partner's behavior in unforeseen situations determines outcome. Partner with strong reputation (won't exploit gaps in contract) even if terms slightly worse. Example: AWS long-term contracts with startups—AWS could exploit pricing gaps (startup grows 100×, pricing locked at startup tier), but doesn't (reputation for supporting customers through growth). Reputation capital enables incomplete contracts to work.

For Strategy Teams: Governance structure choice = how to handle incompleteness. Market transaction (complete contract, arms-length). Strategic alliance (incomplete contract, joint governance). Merger (unified control, no contract needed). Choose based on: (1) Uncertainty (high uncertainty = incomplete contracts inevitable = alliance or merger), (2) Asset specificity (specific investments = need governance, not market), (3) Frequency (repeated interaction = reputation works, one-time = complete contract needed). Disney-Pixar started as incomplete contract (distribution deal), became merger when incompleteness too costly.

Managing Contract Incompleteness Accept incompleteness: Stop trying to specify everything (impossible and expensive) Governing principles: Define decision rights, dispute resolution, renegotiation triggers Partner selection: Choose partners with aligned incentives, reputation for fairness, long-term orientation Governance structure: Joint boards, advisory committees, escalation paths for unspecified situations Flexibility clauses: "Force majeure" (unforeseen events), "material change" (renegotiation triggers), "good faith" obligations Example clauses: "Parties agree to renegotiate in good faith if market conditions change by >30%"

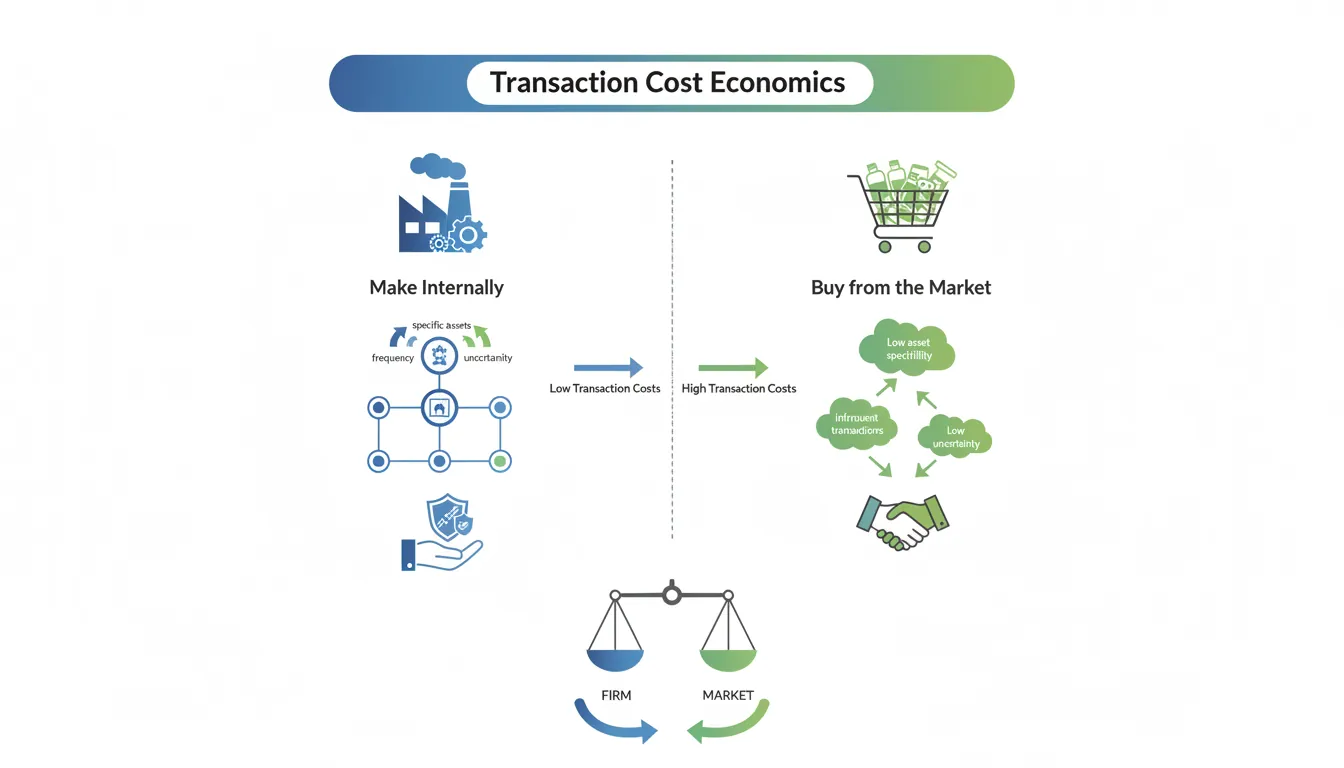

Transaction Cost Economics: Firms Exist to Reduce Friction

Core Principle: Firms exist because market transactions have costs (search, negotiation, contracting, monitoring, enforcement). When transaction costs > coordination costs (managing internally), activity moves inside firm. Explains firm boundaries—why companies make vs. buy, when to vertically integrate, why hierarchies exist.

Transaction cost economics explaining when firms should make internally versus buy from the market

Real-World Application: Make vs. Buy Decisions

Case Study: Tesla's Vertical Integration

AutomotiveTransaction Costs

Setup: Traditional auto: outsource 70% of parts (engines, electronics, seats, glass). Coordinate via contracts with 1,000+ suppliers. Transaction costs: negotiate contracts, manage quality, coordinate delivery, resolve disputes. Tesla: vertically integrates 50% (batteries, software, motors, seats designed/manufactured in-house). Higher internal coordination costs (more employees, factories), but lower transaction costs (no supplier negotiations, faster iteration, IP control).

Trade-Off Analysis: Outsourcing transaction costs (auto industry): $2,000/vehicle (contracts, logistics, quality audits, warranty disputes). Tesla's internal coordination costs: $1,500/vehicle (employees, facilities, inventory). Tesla saves $500/vehicle through vertical integration. Plus strategic benefits: faster innovation (no supplier negotiation for design changes), IP protection (battery tech in-house), supply chain resilience (less dependent on suppliers).

Result: Tesla's integration strategy profitable when transaction costs high (complex, uncertain, rapidly evolving products like EVs). Traditional auto's outsourcing profitable when transaction costs low (stable, modular, commodity parts like seats, glass). Make vs. buy = minimize total costs (transaction + coordination).

Business Applications

For Procurement Teams: Calculate total cost of ownership including transaction costs. Outsourced software development: $100/hour (appears cheap) + management overhead (defining specs, communication, quality control, rework) = $200/hour all-in. In-house: $150/hour salary + benefits (appears expensive) + low coordination costs (colocated, aligned incentives, IP ownership) = $150/hour all-in. Choose based on total cost, not just price. High-complexity, high-uncertainty work (core product development) = bias toward make. Low-complexity, well-specified work (customer support, payroll) = bias toward buy.

For Strategy Teams: Firm boundaries determined by transaction cost vs. coordination cost trade-off. High transaction costs = vertically integrate (oil companies own refineries, drilling, pipelines). Low transaction costs = outsource (Nike owns brand/design, outsources manufacturing to contractors). Technology reducing transaction costs ? firms becoming smaller, more modular. APIs, cloud platforms, gig economy reduce costs of coordinating external parties. Uber doesn't employ drivers (transaction costs now low enough to coordinate via app). Traditional taxi companies employed drivers (transaction costs too high without technology).

For HR Teams: Employment vs. contracting decision driven by transaction costs. Full-time employee: high coordination costs (salary, benefits, management) but low transaction costs (no negotiation, aligned incentives, firm-specific knowledge). Contractor: low coordination costs (pay per project) but high transaction costs (search, negotiate, monitor quality, no firm loyalty). Use FTE for core, repeated, firm-specific work. Use contractors for peripheral, one-time, generic work. Google: engineers = FTE (firm-specific knowledge), facility management = contractors (generic, easy to specify).

Transaction Cost Framework (Ronald Coase / Oliver Williamson) Transaction costs include: (1) Search (finding partners), (2) Negotiation (contracting), (3) Monitoring (quality control), (4) Enforcement (disputes), (5) Coordination (logistics, communication) Coordination costs include: (1) Management overhead, (2) Bureaucracy, (3) Incentive misalignment, (4) Decision-making delays Make vs. Buy rule: Make if transaction costs > coordination costs. Buy if coordination costs > transaction costs Factors favoring "make": Asset specificity, uncertainty, frequency, complexity, IP sensitivity Factors favoring "buy": Standardization, low uncertainty, economies of scale in supplier market, non-core function

Make vs. BuyVertical IntegrationOrganizational Economics

Renegotiation Equilibrium: Deals Evolve Over Time

Core Principle: Long-term contracts inevitably renegotiate as circumstances change. Smart negotiators anticipate this—structure initial deal to maximize value in renegotiation equilibrium (final steady state after all renegotiations), not just initial terms. Matters most in relationships with switching costs, asset specificity, or repeated interaction.

Real-World Application: Sports Contracts

Case Study: NFL Player Contracts

SportsRenegotiation

Setup: Quarterback signs 5-year, $100M contract (2020). Years 1-2: performs well, becomes All-Pro. But salary locked at $20M/year while market rate for All-Pro QB now $40M (salary cap increased, other QBs got raises). Player threatens holdout—refuses to play unless contract renegotiated. Team's options: (1) Hold firm (lose QB for season, miss playoffs), (2) Renegotiate (increase salary to $35M/year, extend 3 more years).

Renegotiation Equilibrium: Original contract = irrelevant. Player's leverage = team invested millions in building roster around him (specific investment, can't quickly replace). Team's leverage = player's alternative (sit out, sacrifice earnings, damage reputation). Equilibrium: renegotiate to ~$35M (split surplus between player's threat point and team's). Initial contract just determined first 2 years—real value determined through renegotiation.

Key Insight: In any relationship with lock-in (team invested in player, player's skills team-specific), initial contract won't hold. Smart negotiators: structure initial deal to maximize total value creation (knowing you'll split surplus via renegotiation), not maximize initial extraction (triggers hostile renegotiation).

Business Applications

For Dealmakers: Design contracts for renegotiation-friendliness. Include: (1) Explicit renegotiation triggers ("if revenue exceeds $X, revisit pricing"), (2) Escalation clauses (automatic adjustments for inflation, market changes), (3) Performance bonuses (align incentives, reduce conflict in renegotiation). Salesforce enterprise contracts: annual "true-up" meetings where pricing adjusted based on actual usage (above/below forecast). Avoids hostile renegotiation by building flexibility into initial agreement.

For Partnership Teams: Choose long-term partners who will renegotiate fairly. Initial contract matters less than partner's renegotiation behavior. Would you rather have: (1) Amazing initial terms + partner who exploits you in renegotiation, or (2) Okay initial terms + partner who shares surplus fairly? Choose (2). Example: Spotify-record labels. Initial deals terrible for Spotify (70% revenue to labels). But Spotify maintained relationships, renegotiated over time as leverage shifted (Spotify now 30% of labels' revenue). Fair renegotiation preserved partnership.

For Executives: Model long-term deals based on renegotiation equilibrium, not initial terms. M&A earnouts: "We'll pay $50M upfront + $50M if revenue hits $100M in year 3." Sounds like $100M deal, but if revenue hits $90M, seller will renegotiate ("We were close, pay $40M extra"). Real expected price: $90M (initial + renegotiation). Budget for renegotiation in financial models—initial deal terms are opening bid, not final price.

Structuring for Renegotiation Accept inevitability: Long-term deals WILL renegotiate (circumstances change, information revealed) Build in flexibility: Escalation clauses, performance adjustments, periodic reviews Explicit triggers: Define conditions that trigger renegotiation (revenue thresholds, market changes, force majeure) Relationship capital: Invest in relationship quality—makes renegotiation collaborative, not adversarial Reputation effects: Renegotiate fairly (short-term extraction damages long-term deal flow) Examples: Talent contracts (sports, entertainment), supply agreements, licensing deals, JVs, franchises

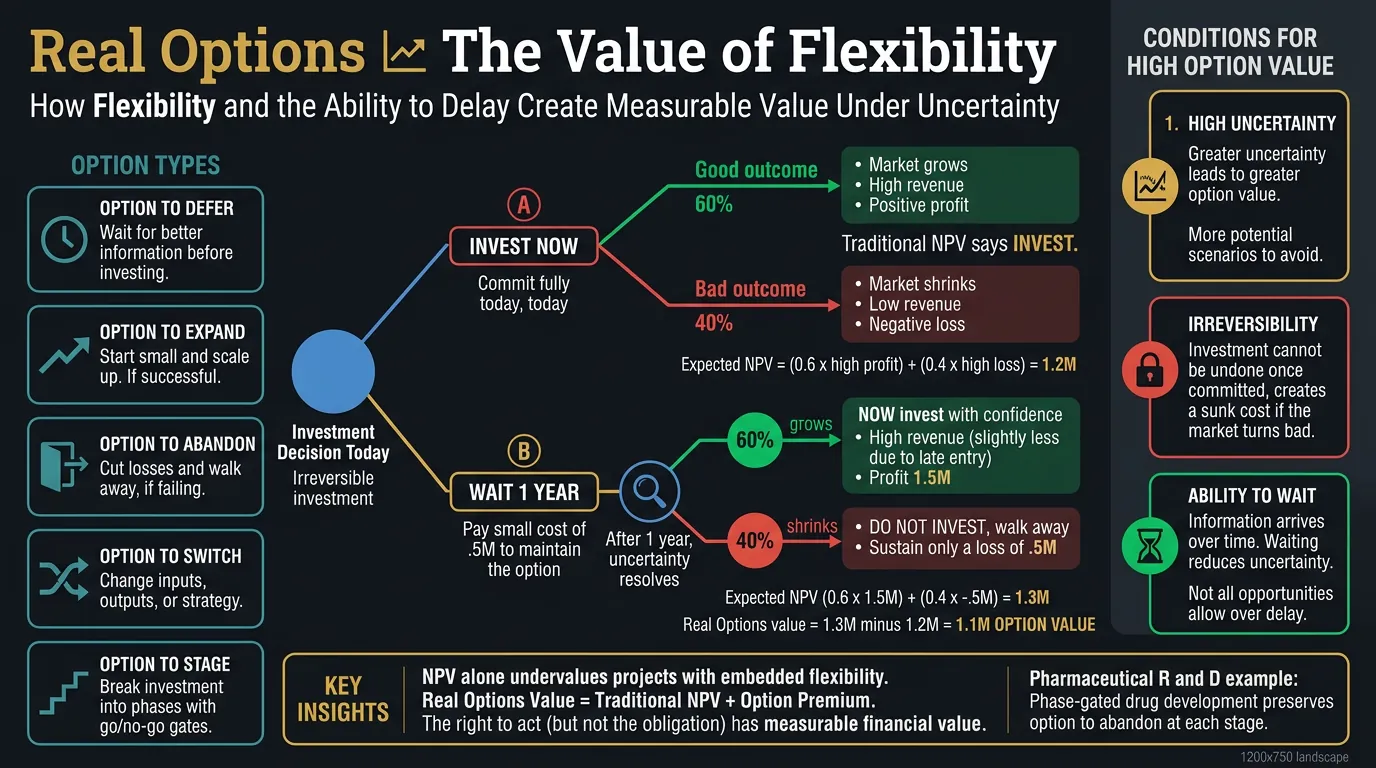

Core Principle: Under uncertainty, flexibility has value. Delaying irreversible decision = keeping options open = option value. Investment decisions should account for option value of waiting, not just NPV. Especially valuable when: (1) high uncertainty, (2) irreversible investment, (3) ability to wait reduces uncertainty.

Real options theory illustrating how flexibility and the ability to delay create measurable value under uncertainty

Real-World Application: Pharmaceutical R&D

Case Study: Phase-Gated Drug Development

PharmaReal Options

Setup: Drug development: Phase 1 (safety, $10M), Phase 2 (efficacy, $50M), Phase 3 (large trial, $200M), FDA approval, commercialization ($500M manufacturing investment). Each phase reduces uncertainty about drug's viability. Traditional NPV: invest $760M upfront, expect $1B revenue ? NPV = $240M. But this ignores option to abandon after each phase.

Real Options Valuation: Phase 1 complete: if promising, proceed to Phase 2 (option value = potential $900M - $50M Phase 2 cost). If unpromising, abandon (save $750M on Phase 2+3+manufacturing). Phase 2 complete: if works, proceed to Phase 3 (option value = potential $700M - $200M). If fails, abandon. Each phase = option to continue OR abandon. Real options NPV: $450M (accounts for flexibility value). Higher than naive NPV because flexibility to abandon bad investments has value.

Key Insight: Phase-gated approach (staged investment with decision points) more valuable than all-at-once investment. Pharmaceutical companies maximize real option value through clinical trial structure—delay irreversible manufacturing investment until uncertainty resolved.

Business Applications

For R&D Teams: Structure innovation as portfolio of options. Early stage: make many small bets (seed funding, pilot projects). Later stage: double down on winners, kill losers. Google's "70-20-10" rule: 70% resources on core business, 20% on related innovations (options on adjacencies), 10% on moonshots (long-dated options on transformative tech). Options portfolio approach beats concentrated betting when uncertainty high.

For Finance Teams: Value flexibility explicitly. Expanding into new market: traditional NPV = -$20M (negative). But real options analysis: pilot launch ($2M) reveals demand, then decide whether to scale ($50M) or abandon. Option to abandon has value—true NPV = -$2M + option value ($15M) = $13M positive. Many "negative NPV" projects become valuable when accounting for flexibility/learning value.

For Strategy Teams: Timing decisions matter. Should you enter market now or wait? Now: capture first-mover advantage but commit resources under uncertainty. Wait: reduce uncertainty (observe competitors, test customer demand) but lose first-mover position. Real options framework: value of waiting = option value - foregone profits from delay. Amazon waited to enter smartphone market (2014, Fire Phone)—value of waiting (observe Apple/Samsung mistakes) exceeded first-mover advantage. Correct decision despite ultimate failure (learned smartphones = commodity, pivoted to Alexa instead).

When Delay Creates Value (Real Options Framework) High option value scenarios: (1) High uncertainty that will resolve over time, (2) Irreversible investment (can't recoup if wrong), (3) Delay doesn't kill opportunity, (4) Low cost of waiting Low option value scenarios: (1) Competitors moving fast (first-mover advantage), (2) Window closing (regulatory changes, market maturity), (3) High cost of delay (foregone profits) Real options in practice: Phase-gated R&D, pilot projects before scale, modular architecture (flexibility to swap components), lease vs. buy (operational flexibility), partnerships before acquisitions Valuation: NPV + option value of flexibility/learning/abandonment

Setup: Intel fab (chip factory): $20B investment, 3-year construction, 10-year depreciation, technology-specific (can't repurpose for different chip architectures). Highly irreversible—if demand doesn't materialize or technology becomes obsolete, $20B loss (equipment has near-zero salvage value).

Decision Threshold: Reversible decision (hiring engineer): invest if expected return >10% (can fire if doesn't work out). Irreversible decision (building fab): invest only if expected return >25% (compensates for irreversibility risk). Intel delays fab investments until: (1) Customer pre-orders secured (demand visibility), (2) Technology validated (Moore's Law trajectory confirmed), (3) Competitor capacity analyzed (no oversupply risk). Irreversibility raises investment bar from "probably profitable" to "highly confident."

Result: Intel's fab investment discipline (only build when demand certain) vs. competitors' overbuilding (build capacity speculatively) gave Intel profitability advantage. Competitors with stranded fabs (GlobalFoundries exited leading-edge manufacturing 2018—$10B+ in sunk fab investments) while Intel maintained 60%+ gross margins through disciplined irreversible CapEx.

Business Applications

For CapEx Decisions: Distinguish irreversible vs. reversible investments. Cloud infrastructure (AWS, Azure): reversible (shut down servers, stop paying monthly). On-premise data center: irreversible ($100M construction, 10-year depreciation). Bias toward reversible when uncertainty high. Netflix: runs entirely on AWS (no data centers)—maintains flexibility to scale up/down based on subscriber growth. Competitors (Comcast) built data centers (irreversible)—stranded assets when cord-cutting accelerated faster than expected.

For M&A Teams: Acquisitions are highly irreversible. Can't "undo" after integration (employees mixed, systems merged, customers migrated). Apply higher evidence threshold: extensive due diligence, pilot integrations (acqui-hires before full merger), performance-based earnouts (delays irreversible payment until results proven). Google's acquisition strategy: small bets ($10-50M acqui-hires, reversible) before large bets ($1B+ acquisitions). Allows learning before committing irreversibly.

For Product Teams: Design for reversibility when possible. Modular architecture: can swap components without redesigning entire system (reversible). Monolithic architecture: components tightly coupled (changes irreversible/expensive). API-first design: can change backend without breaking customer integrations (reversible). Hardcoded integrations: customer dependency locked in (irreversible). Netflix's microservices: each service independently deployable—reversible changes (roll back single service if issues). Monolith: all-or-nothing deploys (irreversible until next release cycle).

Core Principle: Risk = known probabilities (coin flip: 50% heads). Uncertainty = unknown probabilities (new market: ??? % success). Knightian uncertainty = can't even list possible outcomes (Black Swans). Standard decision tools (NPV, probability trees) fail under deep uncertainty. Requires different approach: scenario planning, robust strategies, antifragility.

The spectrum from measurable risk to Knightian uncertainty where probabilities and outcomes are unknown

Real-World Application: COVID-19 Business Impact

Case Study: Pandemic Response Strategies

CrisisKnightian Uncertainty

Setup: January 2020: COVID-19 emerging. Companies face Knightian uncertainty—can't estimate: (1) Severity (mortality rate unknown), (2) Duration (weeks? months? years?), (3) Policy response (lockdowns? travel bans? school closures?), (4) Economic impact (recession depth, recovery timeline). No probability distribution available—fundamentally unpredictable.

Response Strategies: Fragile companies (optimized for efficiency, zero slack): Cruise lines, airlines, malls, theaters—high fixed costs, low cash buffers. Collapsed when revenue ? $0. Robust companies (maintained slack, redundancy): Costco, Amazon, Zoom—cash reserves, flexible cost structures. Survived shock. Antifragile companies (benefited from chaos): Zoom (remote work surge), Peloton (home fitness), Instacart (grocery delivery). Grew 300-500% during crisis.

Key Insight: Under Knightian uncertainty, optimization = fragility. Can't predict specific shock, but can build resilience through: (1) Cash buffers (survive revenue loss), (2) Flexible costs (scale down quickly), (3) Optionality (multiple revenue streams), (4) Antifragile positioning (benefit from volatility). Companies prepared for "unknown unknowns" survived; those optimized for efficiency failed.

Business Applications

For Strategy Teams: Use scenario planning, not forecasts. Knightian uncertainty = can't forecast (probabilities unknown). Instead: imagine multiple futures (best case, worst case, surprising case), design strategy that works across scenarios. Shell pioneered scenario planning (1970s oil crisis)—didn't predict embargo, but prepared for "sudden supply disruption" scenario. When crisis hit, Shell outperformed because strategies pre-designed for that scenario existed.

For Finance Teams: Maintain strategic reserves for unknown unknowns. Standard finance: optimize working capital (minimize cash, maximize leverage). Under Knightian uncertainty: hold excess cash (2-3× normal), maintain undrawn credit lines (backstop liquidity), avoid excessive leverage (debt amplifies shocks). Berkshire Hathaway: $150B cash despite "negative" NPV of holding cash. Rationale: optionality to act when unpredictable opportunities arise (COVID crash, 2008 financial crisis).

For Risk Management: Focus on consequences, not probabilities. Can't estimate probability of unknown unknowns, but CAN estimate maximum tolerable loss. Question isn't "How likely is this?" (unknowable) but "Can we survive if this happens?" (knowable). Nassim Taleb's barbell strategy: 90% in safe assets (survive worst case), 10% in high-risk/high-reward (benefit from positive Black Swans). Middle ground (moderate risk) = vulnerable to unknown unknowns.

Strategies for Unknown Unknowns Scenario planning: Imagine multiple plausible futures, design robust strategies (work across scenarios) Redundancy: Excess capacity, backup suppliers, diversified revenue streams Optionality: Keep options open (don't commit irreversibly), maintain flexibility to pivot Antifragility: Position to benefit from volatility (Taleb's barbell: safe + speculative, avoid middle) Stress testing: Ask "What would kill us?" then ensure those scenarios survivable Examples: Cash reserves (liquidity buffer), supply chain diversity (geopolitical shocks), technology platform flexibility (can migrate if vendor fails)

Core Principle: Rare, high-impact events (outliers) drive disproportionate share of outcomes despite low probability. Normal distributions underestimate tail risk. Examples: 2008 financial crisis, 9/11, COVID-19, dotcom bust. Conventional risk management fails because it assumes "bell curve" world; reality has fat tails (outliers more common than expected).

Real-World Application: Venture Capital Returns

Case Study: Power Law Venture Returns

Venture CapitalBlack Swan

Setup: Typical VC fund: 30 investments, $100M total ($3.3M average). Outcome distribution: 20 companies fail (total loss = $66M), 8 companies return 1-3× ($24M), 1 company returns 10× ($33M), 1 company returns 100× ($330M). Total fund return: $387M on $100M = 3.87× (top-quartile performance).

Black Swan Dominance: Single investment (Facebook, Uber, Airbnb) = 85% of fund returns. 29 other investments = 15% of returns. Fund's success entirely determined by one "Black Swan" winner. Normal distribution thinking: "Diversify to reduce risk, avoid concentration." Power law reality: "Concentrate in potential Black Swans, accept high failure rate." Sequoia's $60M investment in WhatsApp ? $3B return (2014). One investment = 10 years of fund returns.

Key Insight: In fat-tailed domains (tech, media, pharma, entertainment), rare outliers dominate. Optimize for exposure to positive Black Swans (upside optionality), not average-case returns. Peter Thiel: "A great company is a conspiracy to change the world. You want 100× returns, not 2× returns distributed normally."

Business Applications

For Portfolio Strategy: Recognize power law domains vs. normal domains. Power law (Black Swan-driven): tech startups, drug development, oil exploration, movie studios, book publishing. Normal distribution (averages matter): manufacturing, retail, construction, utilities. In power law domains: make many small bets, kill losers fast, double down on winners. Netflix content strategy: green-light 100+ shows/year, cancel 60% after season 1, renew hits for 5+ seasons (Stranger Things, The Crown). Total viewing hours: 80% from top 10% of content (power law). Optimize for hits, tolerate many failures.

For Risk Management: Protect against negative Black Swans, seek exposure to positive ones. Taleb's asymmetry: negative Black Swans (2008 financial crisis) can destroy company. Positive Black Swans (viral product, M&A offer) create upside. Strategy: eliminate catastrophic downside risk (bankruptcy, existential threats) while maintaining upside optionality (experiments, R&D, partnerships). Insurance companies: buy reinsurance for catastrophic events (cap downside), don't hedge moderate losses (expensive, reduces profitability).

For Innovation Teams: Black Swan hunting through experimentation. Can't predict which experiment will 10× business, but can run many experiments cheaply. Amazon: launched 100+ products (Fire Phone, Dash Button, Local Services, Amazon Destinations—all failed). But also launched AWS, Prime Video, Alexa (each $10B+ business). Jeff Bezos: "If you double the number of experiments, you double your invention rate." Black Swan logic: high failure rate acceptable if one success > all failures.

Black Swan Strategy (Nassim Taleb Framework) Negative Black Swans (protect): Financial crisis, pandemic, cyberattack, regulatory change, key person risk. Use insurance, redundancy, scenario planning, stress tests Positive Black Swans (seek): Viral growth, M&A offer, breakthrough innovation, network effects tipping point. Use optionality, experiments, asymmetric bets (small investment, large potential upside) Fat-tailed domains: Tech (winner-take-all), pharma (blockbuster drugs), media (hits-driven), finance (tail risk) Normal domains: Manufacturing, retail, utilities (averages dominate, outliers rare) Strategy: In fat-tailed domains, optimize for Black Swan exposure, not normal returns

Venture StrategyTail RiskPortfolio Approach

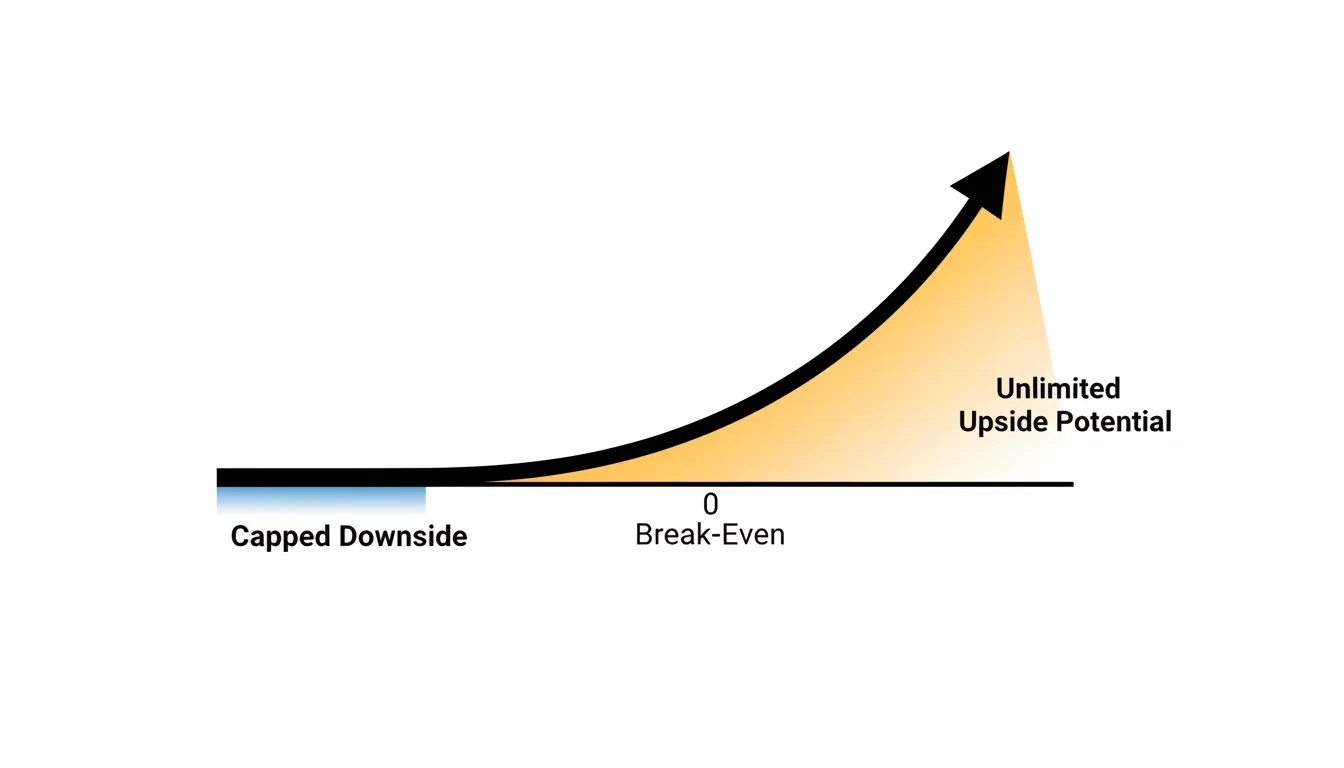

Optionality: Upside > Downside

Core Principle: Optionality = asymmetric payoff (unlimited upside, limited downside). Convex to randomness—benefits from volatility/uncertainty. Seek situations where: (1) Small investment/commitment (capped downside), (2) Large potential payoff (unlimited upside), (3) Multiple paths to success (robust to uncertainty). Startup investing, R&D, partnerships, learning = high optionality.

Optionality showing asymmetric payoff structure with capped downside and unlimited upside potential

Real-World Application: Tech Company Acquisitions

Case Study: Google's Acquisition Strategy

M&AOptionality

Setup: Google acquires 200+ companies (2001-2024). Most are small ($10-100M acqui-hires)—limited downside. Few become massive: YouTube ($1.65B ? $200B+ value), Android ($50M ? dominant mobile OS), DoubleClick ($3.1B ? advertising infrastructure), Waze ($1B ? maps data). Acquisition strategy = portfolio of options.

Optionality Payoff: Downside capped (small acquisitions, can shut down if don't work). Upside unlimited (YouTube alone worth 100× acquisition cost). Asymmetry: 90% of acquisitions contribute little, but 5% generate 1,000× returns. Google doesn't need to predict which acquisitions will succeed—makes many bets, lets winners emerge. Compare to Yahoo: acquired Tumblr $1.1B (2013), wrote down to $230M (2016), sold for $3M (2019). Symmetric bet (large downside, limited upside)—destroyed value.

Key Insight: High-optionality strategy: make many small asymmetric bets (downside capped, upside uncapped). Low-optionality strategy: make few large symmetric bets (equivalent upside/downside). Under uncertainty, optionality dominates forecasting—can't predict winners, but can structure bets to benefit from surprises.

Business Applications

For R&D Teams: Structure innovation as options portfolio. Early-stage R&D: invest small amounts ($50-500K) in many projects (20-50 simultaneously). Downside: lose $500K if project fails (capped). Upside: discover $1B product (uncapped). Kill projects fast when evidence negative (preserve capital for new options). Accelerate when evidence positive (exercise option by scaling investment). Pharma companies: 10,000 molecules in early research ? 100 in preclinical ? 10 in trials ? 1 approved drug. Portfolio of options, not single bet.

For Career Strategy: Build optionality through skills/network. Learning new skill (coding, design, sales): small time investment (100 hours), large potential payoff (new career paths, entrepreneurship opportunities, higher income). Building relationships: low cost (coffee meetings, conferences), high potential value (job offers, partnerships, referrals). Asymmetric: downside = few hours wasted, upside = life-changing opportunities. High-optionality careers (tech, finance, consulting) offer multiple exit paths. Low-optionality careers (academia, government) have limited pivots.

For Strategic Partnerships: Design partnerships as options, not commitments. Start with pilot (small investment, test feasibility). If works, expand to JV (medium investment, shared governance). If massive success, acquire (large investment, full control). Each stage = option to proceed or abandon. Amazon-Whole Foods: started with partnership (Amazon Lockers in stores), expanded to acquisition ($13.7B). Optionality approach: test before commit, scale when proven, avoid large early bets.

Optionality Maximization Framework High-optionality situations: (1) Asymmetric payoffs (small downside, large upside), (2) Multiple paths to success (robust to uncertainty), (3) Learning value (information gain even if fails), (4) Compounding benefits (early investment unlocks future options) Create optionality: Build skills (career flexibility), diversify revenue streams (business resilience), maintain cash reserves (financial options), create partnerships before acquisitions (test before commit) Optionality traps: (1) Too many options = decision paralysis, (2) Free options attract competition (arbitraged away), (3) Optionality valuable only if you CAN act (need resources to exercise options) Examples: Stock options (capped downside = premium, uncapped upside), startup equity (capped downside = time/salary, uncapped upside = IPO), learning (capped downside = time, uncapped upside = career opportunities)

These 10 laws form an integrated system for navigating complex deals and deep uncertainty. The framework has three layers: Deal Structure & Negotiation (optimizing agreements), Strategic Flexibility & Timing (preserving options under uncertainty), and Tail Risk & Antifragility (preparing for unpredictable events). Master this playbook to structure value-creating partnerships, avoid lock-in traps, and thrive in uncertain environments.

Three-Layer Decision Framework Layer 1: Deal Structure & Negotiation - BATNA, hold-up problems, incomplete contracts, transaction costs, renegotiation equilibrium Layer 2: Strategic Flexibility & Timing - Real options theory, irreversibility, when to delay vs. commit Layer 3: Tail Risk & Antifragility - Knightian uncertainty, Black Swan preparation, optionality maximization

Companies that master all three layers: structure better deals, preserve flexibility, survive shocks, capitalize on chaos

Layer 1: Deal Structure & Negotiation Economics

The Five Laws of Deal-Making:

Law

Core Insight

Executive Action

BATNA

Negotiation power = quality of alternatives, not quality of arguments

Improve your BATNA before negotiating; assess counterparty's alternatives to gauge leverage

Hold-Up Problem

Relationship-specific investments create lock-in vulnerability to opportunism

Secure long-term contracts BEFORE making specific investments; use vertical integration or hostage exchanges for protection

Incomplete Contracts

Contracts can't specify all future states; governance structure matters more than contract clauses

Choose partners with reputation for fairness; design governing principles and renegotiation triggers, not exhaustive contingencies

Transaction Costs

Firm boundaries determined by transaction costs vs. coordination costs trade-off

Make vs. buy based on total cost (not just price); vertically integrate when transaction costs high (specificity, uncertainty, complexity)

Renegotiation

Long-term deals inevitably renegotiate; optimize for equilibrium outcome, not initial terms

Build flexibility clauses, escalation triggers, performance bonuses; choose partners who renegotiate fairly over those with best initial terms

Integrated Deal Checklist:

Pre-Deal Due Diligence Questions

BATNA Assessment:

What's our best alternative if this deal fails? (internal development, competitor partnership, stay independent)

What's their best alternative? (assess leverage balance)

Can we improve our BATNA before negotiating? (solicit competing offers, extend runway, develop capabilities)

Lock-In & Hold-Up Risk:

Are we making relationship-specific investments? (custom equipment, dedicated teams, co-located facilities)

How will we protect against post-investment opportunism? (long-term contract, minimum volume guarantees, termination penalties)

Should we vertically integrate instead of outsource? (transaction cost vs. coordination cost analysis)

Contract Incompleteness:

What future states can't we predict? (technology changes, market shifts, competitive dynamics)

How will disputes be resolved? (joint board, arbitration, escalation process)

Does partner have reputation for fairness in unforeseen situations? (check references, past partnerships)

Renegotiation Dynamics:

Will this relationship likely renegotiate over time? (long duration, uncertainty, mutual lock-in = yes)

Have we built in renegotiation-friendly mechanisms? (escalation clauses, performance adjustments, periodic reviews)

Are we optimizing for renegotiation equilibrium or just initial terms? (focus on sustainable long-term structure)

Medium (test with distributors before direct investment)

Proven market demand + local partnerships

Product Launches

Moderately irreversible

Medium (pilot with beta users)

Validated customer demand + unit economics

Cloud Infrastructure

Highly reversible

Low (easy to shut down)

10-15% expected return

Real Options Investment Framework:

When to Delay (High Option Value)

? High uncertainty that will resolve with time (technology maturity, market demand, competitive landscape)

? Irreversible investment (can't recoup sunk costs if wrong)

? Delay doesn't kill opportunity (window stays open, competitors not moving fast)

? Low cost of waiting (foregone profits < option value of learning)

When to Commit Now (Low Option Value)

? First-mover advantages critical (network effects, brand establishment, customer lock-in)

? Window closing (regulatory changes, market maturity, competitive pre-emption)

? High cost of delay (foregone profits, competitor entrenchment, talent acquisition)

? Investment reversible (can scale back if doesn't work)

Phase-Gated Investment Process: Structure major commitments as staged options. Phase 1: Small bet, test critical assumptions ($1-5M pilot). Phase 2: If validated, medium bet to scale proof of concept ($10-50M). Phase 3: If successful, full commitment ($100M+ rollout). Each phase = option to continue or abandon. Preserves flexibility while learning.

Stress Testing: Ask \"What would kill us?\" (customer concentration, key person risk, regulatory change), ensure survivability

Positive Black Swan Exposure (Maximize Asymmetric Upside):

Optionality Portfolio: Make many small bets (R&D projects, partnerships, acqui-hires) with capped downside, uncapped upside

Scalable Revenue Models: Platforms, software, media content scale without proportional cost increases (convex to success)

Strategic Positioning: Trends that could 10× business (AI adoption, regulatory change favoring you, competitor failure)

Acquisition Readiness: Maintain clean cap table, financial transparency, strategic narrative (ready if M&A offer emerges)

Barbell Strategy (Taleb): 85-90% in highly robust activities (protect against negative Black Swans), 10-15% in highly speculative activities with asymmetric upside (benefit from positive Black Swans). Avoid middle ground \"moderately risky\" bets (vulnerable to tail events).

Integrated Case Study: SoftBank's Vision Fund Deal Economics (2017-2024)

How All 10 Laws Interact in Mega-Deals

Venture CapitalIntegrated Framework

Setup: SoftBank raises $100B Vision Fund (2017) for late-stage tech investments. Largest VC fund in history. Strategy: write $1-5B checks into \"category leaders\" (WeWork, Uber, DoorDash, Oyo, ByteDance). Goal: create portfolio of 100× returns (power law venture strategy).

Law #1 - BATNA (Deal Leverage): SoftBank offers $4B to WeWork at $47B valuation (2019). WeWork's BATNA: raise from other VCs at ~$20B valuation (SoftBank offering 2.35× premium). SoftBank's BATNA: invest in other co-working companies or build own. But SoftBank already committed $10B to WeWork (sunk cost, weak BATNA). WeWork's strong BATNA + SoftBank's weak BATNA = WeWork extracts premium valuation + governance control. Outcome: SoftBank overpays, weak deal terms.

Law #2 - Hold-Up Problem (Post-Investment Opportunism): After SoftBank invests $10B in WeWork (relationship-specific, can't redeploy to competitors), WeWork founder Adam Neumann demands: personal loans, real estate deals, family employment. SoftBank locked in (can't abandon $10B), Neumann exploits hold-up (threatens to resign, tank valuation). SoftBank forced to accept unfavorable terms to preserve investment. Outcome: Classic hold-up - specific investment creates vulnerability.

Law #3 - Incomplete Contracts (Governance Failures): SoftBank-WeWork contracts didn't specify: what happens if IPO fails, how to remove founder, path to profitability requirements. When WeWork IPO collapses (2019), no contractual mechanism to force changes. Required emergency renegotiation, boardroom battles, eventually forcing Neumann out through $1.7B golden parachute (incomplete contract = expensive resolution). Outcome: Governance gaps costly when unforeseen situations arise.

Law #4 - Transaction Costs vs. Vertical Integration: SoftBank's model: invest in many portfolio companies, coordinate via board seats (high transaction costs - negotiations, monitoring, conflicts between portfolio companies). Alternative: acquire companies, merge into SoftBank operating divisions (vertical integration - higher coordination costs but aligned incentives). SoftBank chose portfolio approach due to: antitrust concerns (can't merge Uber + Didi + Grab), management complexity (SoftBank lacks operational expertise). Outcome: Transaction cost model appropriate but creates coordination challenges.

Law #5 - Renegotiation Equilibrium: Initial deals with Uber, WeWork, Oyo set at peak valuations (2017-2019). As companies underperform, SoftBank renegotiates: down rounds, additional capital at lower valuations, increased governance rights. Example: Oyo valuation cut from $10B ? $3B in renegotiation. Shows: initial deal terms = starting point, renegotiation equilibrium = true value. Outcome: SoftBank's initial overpayment partially recovered through renegotiation.

Law #6 - Real Options Theory (Staged Investment): SoftBank violated real options logic: instead of small initial bets with options to scale, wrote $1-5B checks upfront (no learning, no flexibility to abandon). Alternative approach: $100M initial ? observe performance ? $1B follow-on if validated. SoftBank's strategy: commit fully to \"category leaders\" without phase-gating. Outcome: Negative option value - locked into large commitments before uncertainty resolved. Vision Fund 1 lost $50B+ on paper.

Law #7 - Irreversibility (Sunk Cost Discipline): WeWork investment highly irreversible: SoftBank can't sell at reasonable price (illiquid market), can't abandon (reputation damage, limited partner pressure). But continues deploying capital to \"protect investment\" (throwing good money after bad). Classic sunk cost fallacy - treating irreversible investment as if still recoverable. Outcome: Total WeWork investment $18B, current value $2B (89% loss).

Law #8 - Knightian Uncertainty (COVID Black Swan): January 2020: Vision Fund portfolio valued at $90B. March 2020: COVID hits, valuations collapse. SoftBank faces Knightian uncertainty - can't predict pandemic duration, economic impact, business model viability (especially travel/office-heavy companies like WeWork, Oyo). Fragile portfolio (high fixed costs, low cash buffers) vs. robust portfolio (asset-light, strong balance sheets). Outcome: Portfolio value drops to $50B (-44%), forced asset sales at distressed prices.

Law #9 - Black Swan Theory (Fat Tails): SoftBank's thesis: venture returns follow power law, one 100× winner covers all losses. Reality: negative Black Swans (WeWork implosion, Greensill collapse) destroyed more value than positive Black Swans (DoorDash IPO, Coupang IPO) created. Exposure to negative tail risk (concentrated bets, leverage, reputation damage) > exposure to positive tail risk (upside capped by IPO timing, market conditions). Outcome: Power law worked against SoftBank - catastrophic losses > mega-wins.

Law #10 - Optionality (Asymmetric Payoffs): Traditional VC: small checks ($10-50M) = capped downside, uncapped upside (asymmetric). SoftBank: $1-5B checks = large downside, upside capped by late-stage entry (asymmetric in wrong direction). Lost optionality benefits - can't make 100 bets at $100M each, instead made 20 bets at $5B each. Portfolio construction destroyed optionality value. Outcome: Symmetric downside/upside = poor risk-adjusted returns.

Key Lessons Integrating All 10 Laws:

Weak BATNA + Hold-Up Vulnerability = Value Destruction: SoftBank's desperate need to deploy capital created weak negotiating position, led to overpaying and being held up post-investment

Incomplete Contracts + Renegotiation = Governance Chaos: Contracts couldn't specify all contingencies, renegotiations became hostile boardroom battles

Ignoring Real Options + Irreversibility = Inflexibility: Large upfront commitments without staged learning destroyed option value and created irreversible losses

Fragility to Black Swans + Wrong Optionality Structure = Catastrophic Losses: Concentrated bets with large downside exposure = portfolio vulnerable to negative tail events

What SoftBank Should Have Done (Framework Application):

BATNA Optimization: Diversify LP base, avoid desperation to deploy capital, maintain alternative investment options

Hold-Up Protection: Tie funding tranches to milestones, governance rights BEFORE large investments, minority rights protections

Real Options: $100M initial ? stage-gate to $1B+ based on performance, preserve abandonment options

Irreversibility Discipline: Avoid sunk cost fallacy, cut losers early even after large investment

Black Swan Preparation: Diversify across sectors/geographies, stress test portfolio for tail events, maintain cash buffers

Optionality Portfolio: Many small asymmetric bets (50 companies × $200M) vs. few large symmetric bets (20 companies × $5B)

Seven Common Executive Mistakes in Deal-Making & Uncertainty Management

Mistake

Why It Happens

Consequence

How to Avoid (Law Application)

1. Negotiating with Weak BATNA

Urgency, desperation, lack of alternatives

Overpay, accept unfavorable terms, weak governance rights

Improve BATNA before negotiating - solicit competing offers, extend runway, develop internal capabilities. Never show desperation.

2. Ignoring Hold-Up Risk

Focus on upfront deal terms, not post-investment dynamics

Counterparty exploits lock-in, extracts value through renegotiation

Secure protections BEFORE specific investment - long-term contracts, minimum commitments, termination penalties. Consider vertical integration.

3. Overspecifying Contracts

Legal teams try to cover every contingency

High legal fees, false sense of security, hostile renegotiation when gaps emerge

Accept incompleteness, focus on governance structure and partner selection over exhaustive clauses. Build renegotiation-friendly mechanisms.

4. Large Irreversible Commitments Under Uncertainty

Pressure to \"move fast,\" fear of missing opportunity

Locked into failed investments, can't pivot when evidence changes

Phase-gate investments - small pilot ? medium scale ? full rollout. Preserve abandonment options. Apply higher decision threshold for irreversible choices.

5. Sunk Cost Fallacy (Throwing Good Money After Bad)

Emotional attachment, loss aversion, reputation concerns

Escalating commitment to failing initiatives, capital trapped in low-return assets

Recognize sunk costs are irrelevant to forward-looking decisions. Cut losers early even after large investment. Focus on incremental ROI, not recovering past spending.

6. Optimizing for Average Case, Ignoring Tail Risk

Bell curve thinking, traditional risk models underestimate fat tails

Fragility to Black Swan events - catastrophic losses when outliers occur

Stress test for extreme scenarios, eliminate catastrophic downside, build redundancy and cash buffers. Ask \"What would kill us?\" and ensure survivability.

7. Destroying Optionality Through Premature Commitment

Pressure to \"decide now,\" fear of seeming indecisive

Lose flexibility value, locked into suboptimal path before learning

Value delay explicitly - calculate option value of waiting vs. cost of foregone profits. Maintain strategic flexibility through pilots, partnerships before acquisitions, reversible architecture.

Master's Checklist: Executives who internalize these 10 laws systematically outperform in deal-making, strategic partnerships, and navigating uncertainty. They structure win-win agreements by improving BATNA and designing renegotiation-friendly contracts. They protect against lock-in through hold-up safeguards and incomplete contract governance. They preserve flexibility through phase-gated investment and real options thinking. They prepare for tail risk through stress testing and optionality portfolios. The result: value-creating deals, strategic adaptability, and organizational resilience in unpredictable environments.

Team Applications: Deal Economics & Risk Management Across Functions

Negotiation and risk management principles apply differently across business functions. This section translates the 10 laws into actionable playbooks for Corporate Development, Finance, Procurement, Sales, and Strategy teams. Each function faces unique deal dynamics and uncertainty challenges—understanding how to apply BATNA optimization, hold-up protection, real options thinking, and Black Swan preparation creates competitive advantage in their domain.

1. Corporate Development & M&A Teams

Core Responsibility: Structure acquisitions, partnerships, and divestitures that create shareholder value while managing integration risk and cultural fit.

Law

Corp Dev Application

Tactical Playbook

BATNA

Strengthen negotiating position through competitive tension and organic alternatives

Multi-Bidder Strategy: Always have backup targets in each category (if acquiring AI startup, negotiate with 2-3 simultaneously). Shows target you have alternatives, improves pricing. Build vs. Buy Analysis: Present credible internal development option (even if slower) to demonstrate BATNA. Reduces target's leverage. Timing Flexibility: Never communicate urgency. Maintain posture that \"we can wait for right deal\" even if board pushing for acquisition.

Hold-Up Problem

Protect against post-acquisition value extraction and key person risk

Earnout Structures: 30-40% of purchase price tied to post-acquisition performance (protects against founder shirking or key employee departure). Lock-up Periods: 3-4 year vesting for acquired founders/teams (prevents immediate departure after payout). Integration Milestones: Release additional capital only after specific milestones met (product integration, revenue targets, customer retention). Governance Rights: Board seats, veto rights on key decisions before acquisition closes.

Incomplete Contracts

Design M&A agreements that handle unforeseen integration challenges

Material Adverse Change (MAC) Clauses: Explicit termination rights if target's business deteriorates pre-close. Reps & Warranties Insurance: Transfer risk of undisclosed liabilities to insurer (avoids post-close disputes). Integration Governance: Joint steering committee (acquirer + acquired execs) meets weekly for first 6 months, monthly thereafter (handles integration issues not specified in agreement). Dispute Escalation Path: Issues ? Integration Lead ? Steering Committee ? CEO ? Board (clear mechanism vs. litigation).

Real Options

Phase-gate M&A from partnerships ? minority investment ? acquisition

Partnership-First Model: Start with commercial partnership (test cultural fit, value creation). Acqui-Hire ? Acquisition: Hire 5-10 key employees first ($2-5M), observe integration for 12 months, then acquire entire company if successful ($50-100M). Reduces irreversibility risk. Minority Stakes: Invest 10-20% via equity round, get board observer seat, option to acquire at pre-negotiated multiple in 18-24 months. Learning period before full commitment. Examples: Salesforce's Slack acquisition ($27B, 2021) - first integrated via partnership, then acquired after observing product-market fit.

Optionality

Build M&A pipeline as portfolio of options, not binary decisions

20 Targets per Year Model: Track 20 potential acquisitions, engage deeply with 5, LOI with 2, close 1. Preserves optionality (never dependent on single deal). Scatter-Gather Approach: Make 10 small acqui-hires ($5-10M each) annually vs. 1 large acquisition ($100M). Capped downside per bet, learn which teams/tech integrate well, double down on winners. Term Sheet Flexibility: Negotiate with multiple targets simultaneously, only sign LOI when terms exceptional (asymmetric payoff). Walk-Away Discipline: Set valuation ceiling based on NPV, walk away if exceeded (avoid winner's curse). 80% of pursued deals should NOT close (shows discipline).

Corp Dev Deal Scorecard Strong Position (Proceed): Multiple viable targets, credible build option, target needs liquidity, cultural fit validated through partnership, earnout structure protects downside Weak Position (Delay/Walk): Single target (no BATNA), target has other suitors, rushed timeline, founder retention critical but not locked up, no integration pilot completed Red Flags: Founder demanding control post-acquisition, material issues discovered in DD without MAC clause, key customers concentrated/at risk, technology integration uncertain

2. Finance & Treasury Teams

Core Responsibility: Optimize capital structure, manage financial risk, value investments under uncertainty, and preserve strategic flexibility.

Law

Finance Application

Tactical Playbook

Transaction Costs

Total cost of ownership analysis including hidden costs of outsourcing vs. in-house

Make vs. Buy (Finance Functions): Outsourced accounting: $150/hour billing + management overhead (defining requirements, reconciling errors, security compliance) = $250/hour all-in. In-house: $120/hour fully loaded + direct control + no coordination lag = $120/hour. Choose based on total cost, not sticker price. Technology Build vs. Buy: Off-shelf ERP: $500K license + $300K implementation + $200K annual maintenance + $100K customization = $1.1M year 1, $300K ongoing. Custom build: $800K development + $150K maintenance = $950K year 1, $150K ongoing. Factor in switching costs (data migration, retraining). Rule: Standardized, high-frequency tasks (payroll, expense management) = buy. Firm-specific, strategic functions (FP&A models, treasury management) = build.

Real Options

Value flexibility in investment decisions (pilot before scale, lease vs. buy, staged CapEx)

Real Options NPV Model: Traditional NPV ignores flexibility value. Project with -$5M NPV may have +$10M NPV when accounting for option to expand if successful, abandon if failing. Formula: NPV = Base NPV + Option Value (Expansion) - Option Cost (Delay). Lease vs. Buy (Equipment): Lease: higher monthly cost but preserves option to upgrade, downsize, or exit. Buy: lower total cost but irreversible commitment. Choose lease when technology uncertainty high (rapid obsolescence), demand uncertainty high (might not need capacity), or capital constrained (preserve liquidity). Modular CapEx: Instead of $50M factory built upfront, design for $10M initial capacity + 4× $10M expansion modules. Preserves option to stop after Phase 1 if demand doesn't materialize.

Irreversibility

Apply higher hurdle rates for irreversible investments (CapEx, acquisitions) vs. reversible (R&D, cloud)

Tiered Hurdle Rates: Reversible investments (marketing, contractors, cloud): 10-12% IRR threshold. Moderately irreversible (hiring, product launches): 15-18% IRR. Highly irreversible (factories, acquisitions, geographic expansion): 25-30% IRR + demand certainty. Compensates for inability to recoup if wrong. CapEx Stage-Gating: $100M factory investment: Phase 1 feasibility study ($2M), Phase 2 engineering design ($5M), Phase 3 site preparation ($10M), Phase 4 construction ($83M). Decision gate after each phase—option to abandon if demand forecast changes. Pre-Sales for CapEx: Secure customer pre-orders for 60-80% of capacity before committing to factory construction (reduces demand uncertainty for irreversible investment).

Knightian Uncertainty

Stress test financial resilience to unknown unknowns (recession, pandemic, regulatory shocks)

Liquidity Stress Testing: Model scenarios: (1) Revenue drops 40% for 12 months, (2) Major customer churns, (3) Supply chain disrupted for 6 months, (4) Credit markets freeze. Ensure company survives all scenarios with cash + undrawn credit. Target: 18-24 months runway under worst case. Debt Maturity Laddering: Avoid concentration (don't have 50% of debt maturing in single year). Ladder maturities 3-5-7 years (if recession hits, not forced to refinance entire debt stack at distressed rates). Covenant Headroom: Negotiate debt covenants with 30-40% buffer (leverage ratio max 4.0×, maintain at 2.5-3.0×). Avoids covenant violations in moderate downturns. Strategic Reserves: Hold 2-3× normal working capital in cash/equivalents (Knightian uncertainty buffer for unpredictable shocks).

Black Swan

Portfolio approach to risk - protect against negative tail events, seek positive tail exposure

Tail Risk Hedging: Use catastrophe bonds, put options, gold/treasuries to hedge extreme market events (2008-style crashes). Cost: 1-2% of portfolio annually. Benefit: 20-50% protection in tail event. Insurance against negative Black Swans. Asymmetric Upside Exposure: Allocate 5-10% of investment portfolio to venture capital, growth equity, strategic options (M&A targets, emerging markets). Capped downside (can only lose invested capital), uncapped upside (could 10-100× in positive Black Swan). Currency Diversification: Don't hold 100% of reserves in single currency (USD, EUR). Diversify 20-30% into alternatives (CHF, gold, Bitcoin) as tail risk hedge against fiat devaluation. Example: MicroStrategy's Bitcoin strategy (2020-2024) - allocated 10% of treasury reserves to BTC. Result: $5B investment ? $15B value (positive Black Swan exposure).

Finance Risk-Adjusted Decision Framework Reversible + Low Uncertainty: Standard NPV at 10-12% hurdle rate (cloud infrastructure, marketing campaigns) Moderately Reversible + Medium Uncertainty: Real options NPV at 15-18% hurdle rate + pilot phase (product launches, partnerships) Irreversible + High Uncertainty: Stress-tested NPV at 25-30% hurdle rate + demand validation (CapEx, M&A) Knightian Uncertainty: Scenario analysis (not probabilistic), ensure survivability in worst case, barbell approach (safe + speculative)

3. Procurement & Supply Chain Teams

Core Responsibility: Optimize supplier relationships, negotiate contracts that balance cost with risk, and build resilient supply chains.

Law

Procurement Application

Tactical Playbook

BATNA

Create competition among suppliers to improve pricing and terms

Multi-Source RFPs: Never sole-source critical components. Solicit bids from 3-5 qualified vendors even if preferred supplier known (competition improves pricing 15-30%). Second-Source Qualification: Even if using primary supplier for 80% of volume, maintain qualified second source for 20% (BATNA if primary fails to deliver or price gouges). Cost: 2-3% price premium for split volume. Benefit: leverage in renegotiations + supply continuity. In-House Capability Threat: For strategic components, develop internal prototyping capability. Shows suppliers you can build internally if priced unreasonably (credible BATNA even if not economical to produce at scale). Example: Apple designs its own chips in-house (improves BATNA with TSMC for manufacturing - can threaten to switch fabs if pricing unfair).

Hold-Up Problem

Protect against supplier opportunism after you've committed to their components

Long-Term Contracts BEFORE Lock-In: If making supplier-specific investments (custom tooling, dedicated production line, co-location), negotiate 3-5 year contracts with price caps BEFORE investment. Prevents hold-up after sunk cost committed. Volume Commitments with Price Protection: \"We guarantee 10,000 units/month minimum for 3 years at $X/unit, escalating with CPI max 3%/year.\" Supplier gets volume certainty, you get price protection. Dual Sourcing Critical Parts: Split orders 60/40 between two suppliers for mission-critical components. Prevents either from holding you up (can shift volume to alternative). Cost: lose volume discounts. Benefit: supplier discipline. Escrow Source Code/Tooling: For custom software or tooling, hold source code/designs in escrow (release if supplier fails to support or tries hold-up). Reduces lock-in leverage.

Renegotiation

Design supplier contracts for fair renegotiation as circumstances change

Price Escalation Clauses: \"Raw material cost increases >10% trigger quarterly price review.\" Allows fair renegotiation if supplier's input costs spike (avoids adversarial renegotiation or supplier bankruptcy). Volume Flexibility Bands: \"Committed volume 8,000-12,000 units/month at $X. Below 8,000 = +5% price, above 12,000 = -5% price.\" Handles demand volatility without full contract renegotiation. Annual True-Ups: Contract includes mandatory annual review of pricing vs. market rates, volume actuals vs. forecast, quality metrics. Adjust pricing ±10% based on performance. Avoids hostile renegotiation by building flexibility into initial agreement. Force Majeure + Renegotiation: If extreme events (pandemic, trade war, natural disaster), explicit clause triggering good-faith renegotiation vs. termination. Preserves relationship while adapting to changed circumstances.

Transaction Costs

Make vs. buy decisions accounting for search, negotiation, monitoring, and quality control costs

Total Cost of Outsourcing: Off-shore manufacturing: $10/unit (appears cheap) + shipping ($1), tariffs ($0.50), quality control ($0.80), inventory carrying costs (longer lead times, $1.20), supplier management/audits ($0.50), IP risk/legal ($0.30) = $14.30 all-in. Domestic: $13.50/unit fully loaded. Choose domestic despite higher \"price\" due to lower transaction costs. Supplier Consolidation: 100 suppliers = high transaction costs (100 contracts to negotiate, 100 quality audits, 100 payment processes). Consolidate to 20 strategic suppliers—increases volume per supplier (better pricing), reduces overhead (fewer contracts/audits). Vertical Integration for Critical Components: If transaction costs (quality variability, delivery unreliability, IP concerns) > coordination costs (managing internal manufacturing), bring in-house. Example: Tesla batteries—initially outsourced to Panasonic, vertically integrated when transaction costs exceeded internal coordination costs.

Optionality

Build supply chain flexibility to adapt to disruptions and demand volatility

Geographic Diversification: Don't concentrate 80% of supply in single country/region (China risk, tariff risk, geopolitical risk). Spread across 3+ regions (Asia 50%, Europe 25%, Americas 25%). Cost: 3-5% efficiency loss. Benefit: optionality if one region disrupted. Inventory Buffers for Critical Parts: For long-lead-time, single-source components, hold 90-120 days safety stock (vs. normal 30 days). Cost: working capital tied up. Benefit: option to survive supplier disruption without production halt. Flexible Manufacturing (Postponement): Design products with common platform, late-stage customization. Allows holding generic inventory, customizing based on actual demand. Preserves demand flexibility (optionality to respond to market shifts). Supplier Development Programs: Invest in developing new suppliers (technical support, volume ramps) even if current supplier performing well. Builds optionality for future (if current supplier becomes unreliable, qualified alternatives ready).

Procurement Negotiation Checklist Pre-Negotiation: Identify BATNA (alternative suppliers, in-house option), assess supplier's BATNA (are we critical customer?), map hold-up risks (specific investments on either side) Contract Structure: Long-term commitment + price protection for lock-in situations, volume flexibility bands, escalation clauses for input cost changes, annual review triggers Risk Mitigation: Dual-source critical components, escrow tooling/IP, reps & warranties on quality/delivery, termination rights if supplier financial distress Flexibility Mechanisms: Force majeure with renegotiation clause, demand variability bands, geographic diversification requirements

4. Sales & Business Development Teams

Core Responsibility: Win enterprise deals, negotiate pricing and terms that balance revenue with customer success, and build long-term strategic partnerships.

Law

Sales Application

Tactical Playbook

BATNA

Strengthen negotiating position by understanding and improving customer's alternatives

Assess Customer's BATNA: Strong BATNA (incumbent solution working well, multiple vendors competing) = must offer compelling ROI + differentiation. Weak BATNA (legacy system failing, urgent deadline, switching costs high) = pricing power increases. Discovery: \"What's your current solution? Evaluated other vendors? What happens if you don't implement new system this year?\" Reveals BATNA strength. Improve YOUR BATNA: Maintain healthy pipeline (if dependent on single mega-deal, customer has leverage). Rule: No single deal should be >20% of quarterly quota (preserves walk-away power). Competitive Bake-Offs: If customer running bake-off with 3 vendors, differentiate on dimensions where competitors can't match (integration, support, roadmap alignment). If can't win on those, walk away (avoid price war where only customer wins).

Hold-Up Problem

Avoid creating customer lock-in that enables renegotiation pressure post-sale

Transparent Pricing: If your SaaS product has high switching costs (data migration pain, retraining costs, workflow dependencies), don't exploit lock-in through aggressive price increases. Customer resents hold-up, churns when alternative appears. Instead: predictable escalation (CPI + 3% annually), volume discounts for growth (align incentives), multi-year discounts (lock in fair pricing long-term). Avoid Hostage Situations: Don't design contracts where customer trapped with unfair terms post-implementation. Example: \"$50K setup fee, then $500K/year subscription.\" After paying $50K sunk cost, customer held up for $500K subscription. Better: \"$30K setup included in year 1, $300K total first year, $270K ongoing.\" Fair pricing avoids resentment. Success-Based Pricing: Tie pricing to customer outcomes (\"we only earn renewal if you achieve ROI\"). Shows confidence, avoids hold-up perception. Example: Snowflake's consumption-based pricing - customers pay for usage, not locked into flat fees. Reduces hold-up friction, drives retention.

Incomplete Contracts

Design enterprise contracts that handle scope changes and unforeseen requirements

Flexible Scope Definitions: Enterprise software contracts can't specify every feature request. Include: \"Roadmap items subject to change based on product strategy and customer feedback. Customer may submit feature requests via product council.\" Governance mechanism (product council) handles incompleteness vs. rigid contract. Change Order Process: Material scope changes (new integrations, custom development, additional modules) trigger change order process: estimate effort, agree on pricing, amend SOW. Prevents disputes when requirements evolve. Annual Business Reviews: Mandatory quarterly or annual reviews where both parties align on: product adoption, success metrics, upcoming needs, pricing adjustments. Handles incompleteness through ongoing dialogue vs. static contract. Exit Clauses: If partnership not working (both parties frustrated), explicit exit mechanism with data portability, transition support, pro-rated refunds. Better to part ways amicably than force failing relationship.

Renegotiation

Structure deals anticipating renewal and expansion negotiation

Land-and-Expand Pricing: Initial deal: 100 seats at $100/user/month = $120K annual contract. Year 2 expansion: 500 seats. Don't renegotiate from scratch—honor year 1 pricing for original 100 seats, negotiate incremental 400 seats at $90/user (volume discount). Smooth expansion vs. hostile renegotiation. Multi-Year with Expansion Options: \"3-year contract at $500K/year, customer has option to add modules (CRM, analytics, workflow) at pre-negotiated pricing.\" Customer gets predictability, you get expansion revenue without full renegotiation. Success-Based Escalation: \"If customer achieves >$5M revenue impact from our product, pricing increases to $800K/year (vs. $500K baseline).\" Aligns incentives, renegotiation built into value creation. Avoid All-or-Nothing Renewals: Subscription businesses: don't make renewal binary (renew or churn). Offer tiered options (downgrade to basic tier, pause subscription, reduce seats). Preserves relationship, revenue even if customer reducing spend.

Optionality

Build strategic partnerships as options that can expand or contract based on success

Pilot-First Approach: Enterprise deals: start with 3-month pilot (20% of full scope, $50K vs. $500K multi-year). Customer learns if solution works, you learn if customer good fit. Option to expand to full deal if successful, abandon if not (capped downside, preserves upside). Modular Contracting: Don't force customers to buy full suite upfront. Core product ($200K) + optional add-ons (analytics +$50K, AI module +$80K, premium support +$30K). Customer starts small, adds modules as value proven. You preserve expansion optionality. Strategic Partnership Tiers: Tier 1 (Pilot): 3-month trial, limited scope, monthly billing. Tier 2 (Growth): Annual contract, core product, success metrics tracking. Tier 3 (Strategic): Multi-year, full suite, executive sponsorship, co-innovation. Allows relationship to scale based on mutual success. Example: Stripe's developer-first approach - free to start, pay as you grow. Optionality drives adoption, expands with customer success.

Sales Deal Quality Scorecard High Quality Deal (Green Light): Customer has strong business case (clear ROI), champion with budget authority, weak BATNA (urgency to solve problem), multi-year commitment with expansion potential, fair pricing (not race-to-bottom discount) Medium Quality (Proceed with Caution): Budget uncertain, competitive situation (strong customer BATNA), single-year deal, requires heavy customization, pricing pressure Low Quality (Red Flag / Walk Away): Customer has strong alternative, no urgency, discount expectations unrealistic, scope creep likely, credit risk concerns, misalignment on value metrics

5. Strategy & Corporate Planning Teams

Core Responsibility: Shape long-term strategic direction, evaluate market entry and exit decisions, and build organizational resilience to uncertainty.

Law

Strategy Application

Tactical Playbook

Real Options

Structure market entry, product launches, and geographic expansion as staged options